Mission 300 has committed over $50 billion since July 2023 to connect 300 million people across Sub-Saharan Africa by 2030. Governments have signed compacts. A Private Sector Council has been established and is mobilising capital. Targets are published, reform priorities declared, and the initiative has established itself as the continent’s most prominent access platform. The question none of this answers: which countries can convert commitment into actual connections? The variable that sets delivery speed is institutional capacity: the ability to absorb capital, deploy connections, and sustain service. Ambition is visible everywhere. Readiness is not.

Executive Summary

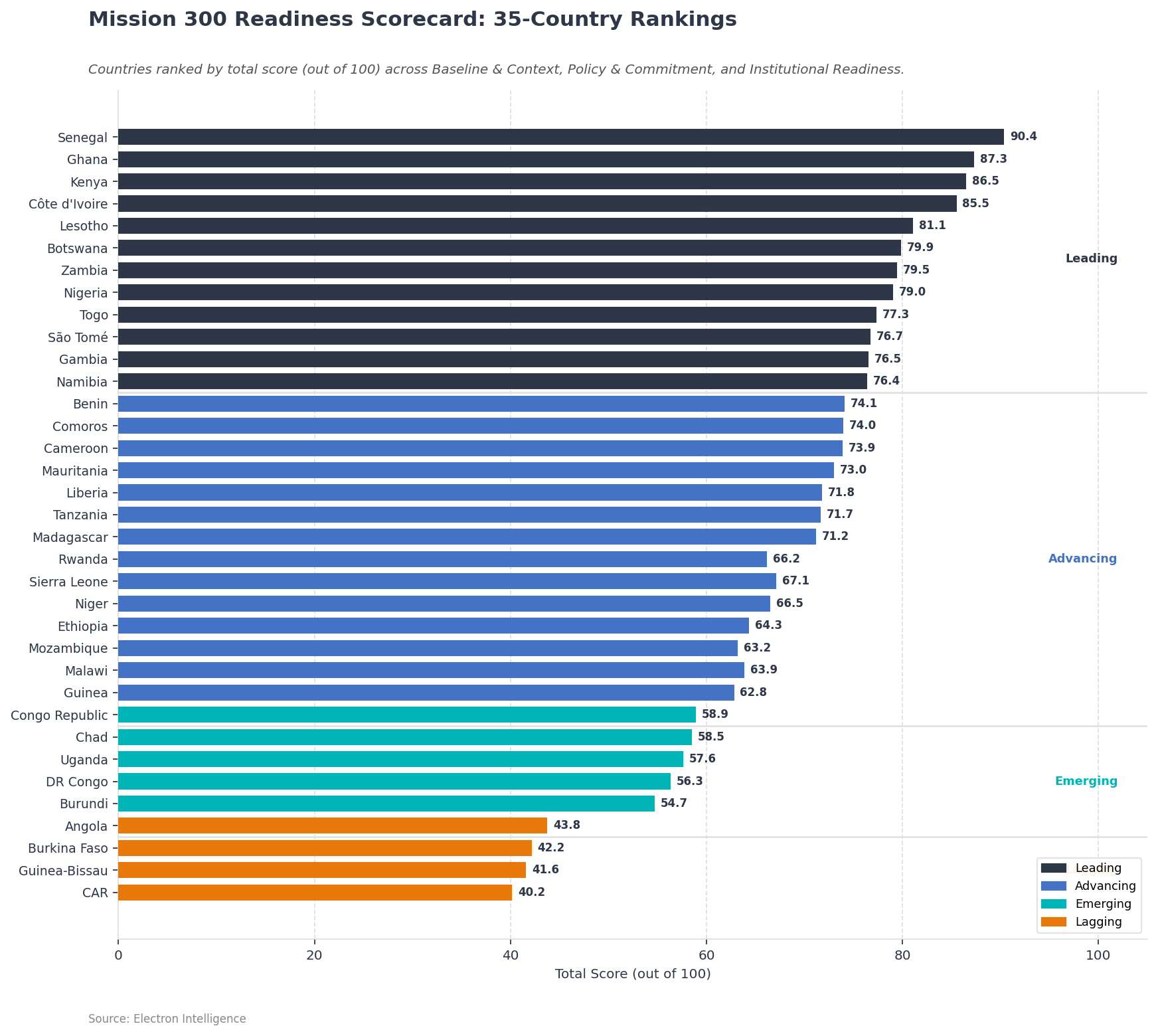

- The readiness scorecard ranks 35 countries across three pillars: Baseline & Context, Policy & Commitment, and Institutional Readiness, out of 100 points. Only 12 countries sit in the Leading tier (≥75). Fourteen are Advancing, five Emerging, and four Lagging.

- Institutional Readiness, running from 16 (Guinea-Bissau) to 37.5 (Senegal), is the widest-spread pillar and the variable most correlated with overall score. Compact signatures alone do not move it.

- The top five: Senegal (90.4), Ghana (87.3), Kenya (86.5), Côte d’Ivoire (85.5), and Lesotho (81.1), combine strong policy commitment with credible delivery architecture. Nigeria and Zambia hold leading positions despite large unelectrified populations.

- The Advancing tier holds countries with potential but a narrower margin for execution. Liberia, Tanzania, Madagascar, Sierra Leone, Niger, and Mozambique carry heavy access burdens that commitment alone cannot resolve.

- Rwanda and Uganda score below their delivery conditions because of the absence of a compact cap; their Policy score is 11. A signed compact would add approximately 15 points to each.

- If lower-readiness countries miss targets, Mission 300 reaches its headline through concentration in a smaller group of stronger markets and off-grid scale-up, not the country-led transformation the compacts were designed to catalyse.

- Countries drawing concessional IDA and ADF capital early without matching delivery will face harder commercial terms later. Angola, Burkina Faso, Guinea-Bissau, and CAR are the most exposed.

- The Mission 300 Private Sector Council signals where private capital is positioned to follow, but only where payment systems, tariff stability, and off-taker arrangements hold.

What the Score Tests

Public signals around Mission 300 carry different weight. Targets indicate intent. Political visibility indicates alignment. Compact activity indicates engagement. None indicate whether a country can convert ambition into connections. A country can be highly visible in the initiative and still face a difficult delivery path. Another can look less prominent politically yet sit on a stronger operational base.

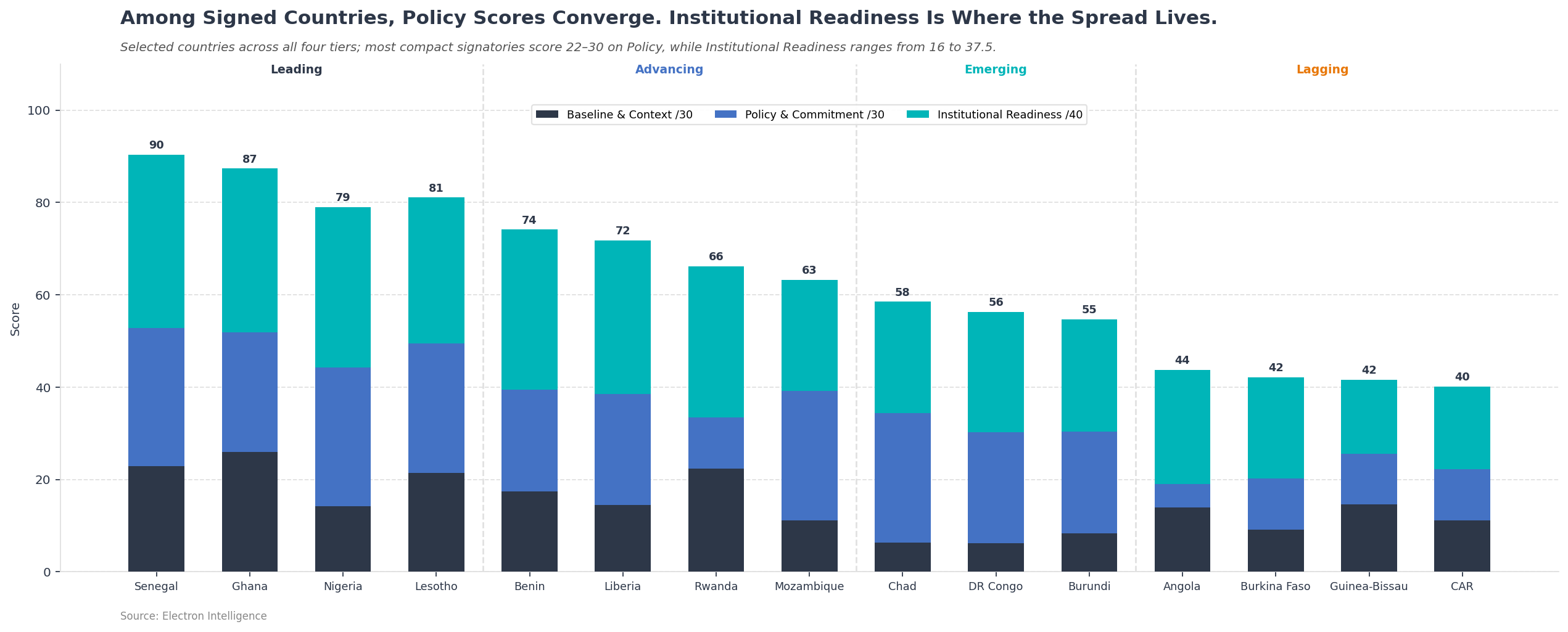

Exhibit 2: Pillar-level scores by country. Institutional Readiness (green) shows the widest spread and tightest correlation with total score.

The scorecard tests three dimensions:

- Baseline & Context: where a country starts, with access rates from 12% in Chad to 90% in Comoros.

- Policy & Commitment: how far the country has moved into the Mission 300 framework through its compact, cohort, and declared targets.

- Institutional Readiness: the enabling environment, drawn from the AfDB Electricity Regulatory Index Composite. Institutional Readiness carries the widest spread and the tightest correlation with total score, running from 16 at Guinea-Bissau to 37.5 at Senegal.

Four Tiers, Four Different Delivery Problems

The scorecard ranks 35 participating countries on Baseline and Context, Policy and Commitment, and Institutional Readiness. Twelve countries sit in the Leading tier, fourteen in Advancing, five in Emerging, and four in Lagging.

The rankings are most useful when read as a map of country situations rather than as a simple league table. The Leading tier contains countries where commitment appears more actionable because the institutional foundation is stronger and the delivery path is more credible. The top five are Senegal (90.4), Ghana (87.3), Kenya (86.5), Côte d’Ivoire (85.5), and Lesotho (81.1). They are followed by Botswana, Zambia, Nigeria, Togo, São Tomé & Príncipe, Gambia, and Namibia, all above 75.

Exhibit 1: Readiness scores across 35 Mission 300 countries. Twelve sit above the 75-point Leading threshold; four score below 50.

These countries do not all look the same. Senegal combines a top institutional score with active implementation support. In March 2026, the World Bank proposed $100 million in additional financing for Senegal’s Energy Access Scale-Up Project, including grid densification, new household connections, technical assistance to Senelec, and a results-based financing mechanism for verified connections. That does not prove Senegal will hit its target. It does show that Dakar has aligned policy intent, utility support, and execution architecture more tightly than most peers.

Ghana and Kenya are strong for different reasons. Ghana’s compact ties universal access to infrastructure modernisation, financing mobilisation, and sector reform. Kenya’s compact places weight on private participation, procurement architecture, and a very large financing programme tied to a 2030 universal-access goal. In both cases, the scores reflect more than the target itself. They capture a broader delivery framework behind it.

Nigeria and Zambia are more demanding tests of the same principle. They still carry much larger unelectrified populations than the smaller leading markets, but they remain in the top tier because policy commitment and institutional readiness line up more credibly than they do in most large-deficit peers. Nigeria’s compact is explicit that delivery depends on financially viable utilities, transmission, and distribution investment, and private-sector participation, while its DARES programme is positioned as a flagship scale-up model for distributed access.

The Advancing tier is larger and less uniform. One group combines serious commitment with a still-heavy access deficit. Liberia, Tanzania, Madagascar, Sierra Leone, Niger, and Mozambique sit here. They have entered the framework, set ambitious targets, and retain enough institutional strength to remain plausible, but their constraint is the size of the delivery task. Tanzania’s compact, for example, explicitly assumes a sharp acceleration in connections relative to the current pace. Tanzania’s constraint is implementation pace, not ambition.

A second group has stronger readiness than its rank suggests. Rwanda and Uganda both have strong access baselines and institutional scores above 31, but sit in the D1 cohort without a compact, capping their Policy score well below signed countries. A compact would add approximately 15 points to each.

In a third group, governments have set targets their institutions cannot yet support. Chad and DR Congo both carry meaningful ambition in the policy pillar but start from very low access bases and thinner institutional platforms. Reaching their 2030 targets would require building more connections than many countries on the list currently have in total. The targets are serious. The delivery paths beneath them are thin. Mozambique is more mixed: enough policy and institutional strength to avoid the bottom tier, but its remaining access burden is large enough that progress depends on execution pace, procurement discipline, and utility performance.

The lower end of the score distribution reflects the hardest combination. The four Lagging countries are Angola, Burkina Faso, Guinea-Bissau, and Central African Republic. All four are D1. None has signed a compact, so their policy scores are capped. Institutional Readiness ranges from weak to very weak. CAR combines very low access with fragility and a thin regulatory base. Angola is a useful contrast. Its access rate and institutional score are materially stronger than the rest of the Lagging group, but the absence of a compact alone pulls the total score well below where its baseline would otherwise place it.

Meet, Miss, or Exceed

No single delivery pattern will work across 35 countries. The ones most likely to meet targets pair ambition with institutional quality. The World Bank’s March 2026 update notes that connection delivery has concentrated in countries with operational Country Delivery Management Units (CDMUs), functioning utilities, and working regulators. CDMUs are operational in Malawi and Nigeria, with others under set-up. Where those conditions hold, the gap between target and plausible execution is narrow.

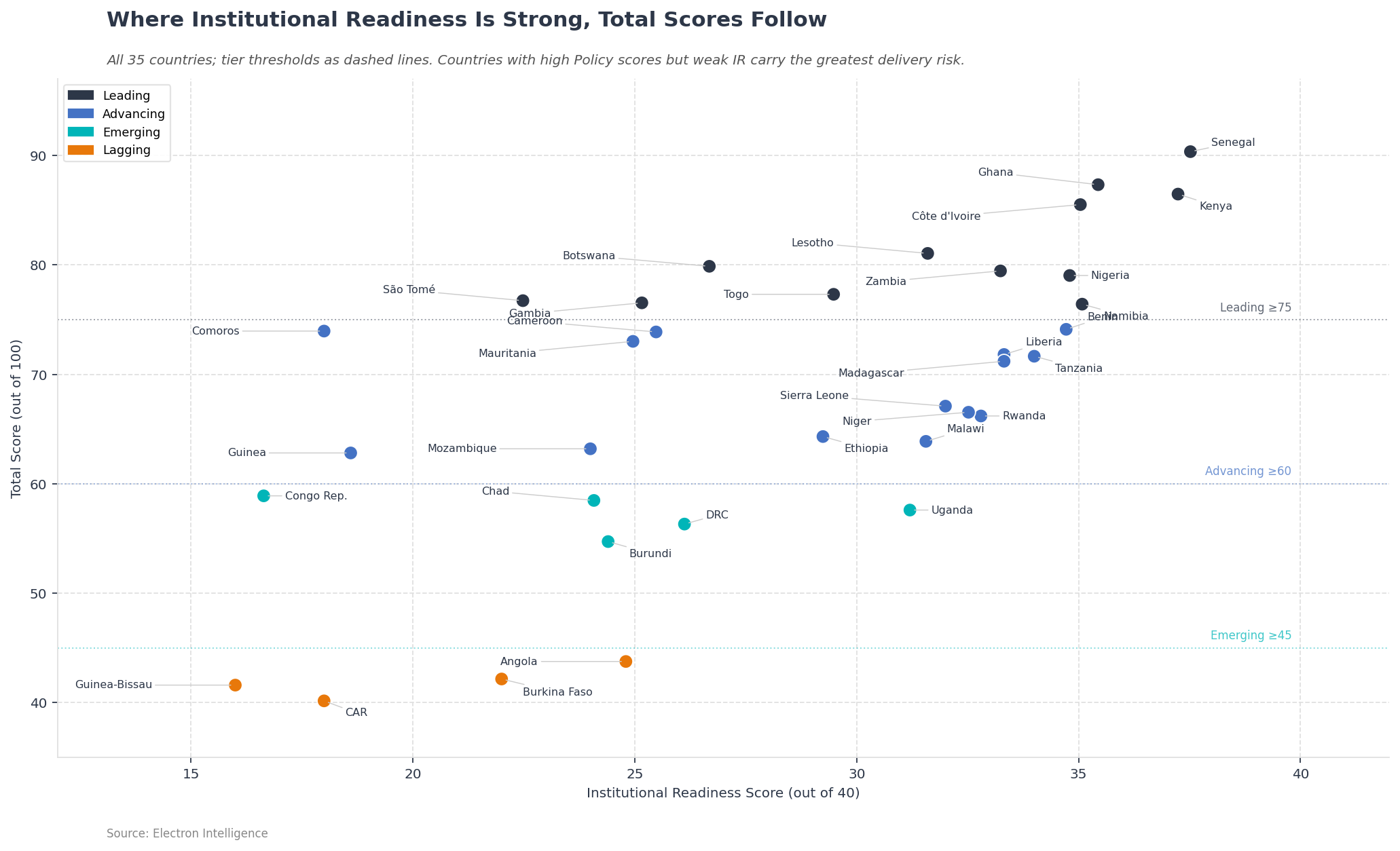

Exhibit 3: Gap-to-target analysis. Countries with high ambition and low institutional readiness face the widest implementation gaps.

Countries miss targets two ways. Institutionally: the target sits above what the enabling environment can support. Structurally: credible intent meets a delivery burden larger than the ambition score suggests. The IEA’s 2025 Outlook quantifies the friction: 600 million people remain unelectrified, progress has stalled since 2019, and Africa attracts 3% of global energy investment against 20% of global population. Targets backed by weak conditions stay aspirational.

Countries near tier boundaries can move up if regulatory execution improves or if grid and distributed solutions scale faster than current conditions suggest. Benin (34.7 on Institutional), Liberia (33.3), Tanzania (34.0), and Madagascar (33.3) hold institutional strength that the overall rank understates. Their constraint is access deficit. Modest implementation gains would move them into the Leading tier within two calibration cycles.

When Countries Miss

Missing targets produces a specific failure mode: the headline advances while the base narrows. Nigeria, Tanzania, Zambia, Mozambique, and the twelve Leading countries hold enough delivery capacity to push the 300 million total. DRC carries over 80 million unelectrified people, Nigeria over 60 million. If those large-population, better-positioned countries accelerate, the continental aggregate looks like progress. The country distribution behind it does not. The World Bank and SEforALL have signalled that off-grid connections, which delivered half of Mission 300 connections to date, will carry more of the incremental load. Mini-grids supply 2 percent of African electricity. Solar home systems reach 4 percent of households. Scaling those channels bypasses weak utilities rather than building them.

A programme that hits aggregate numbers through a smaller, stronger group can preserve momentum in the headline, but it narrows the country story behind it. DRC, Chad, and Mozambique sit at the centre of that tension: heavy targets on thin delivery platforms, with populations large enough to reshape continental progress.

The financing consequence is direct. Mission 300 carries the lowest concessional terms available through IDA and ADF, supplemented by blended finance. Countries that draw that capital early without matching delivery will face harder commercial terms as electrification advances. Angola, Burkina Faso, Guinea-Bissau, and CAR are the most exposed. A readiness gap today becomes a debt burden later.

Where Overperformance Is Likeliest

The likeliest candidates for overperformance sit in the upper Advancing band. Benin, Liberia, Tanzania, and Madagascar hold institutional scores that their overall rank understates. The constraint is scale of the remaining access task, not delivery weakness. Stronger utility performance and faster last-mile rollout would move them into the Leading tier within the next calibration cycle. As noted, Rwanda and Uganda would gain approximately 15 points with a signed compact. Their scores can move faster than those of many signed countries once that formal alignment changes.

For the Leading tier, overperformance takes a different form. Senegal and Ghana have little room to rise in rank. Their scores are near the ceiling. The test is whether they convert readiness into delivery pace: earlier commissioning, fewer implementation delays, and more consistent last-mile progress. If they do, the top tier absorbs an even larger share of Mission 300’s realised connections.

Sustained overperformance depends on conditions that financing alone cannot create. The Mission 300 Private Sector Council, launched in March 2026 under Makhtar Diop of IFC and Ray Chambers of the MCJ Foundation, places 14 private-sector leaders on a shared delivery platform, including the CEOs of Globeleq, M-KOPA, Sun King, and Husk Power. Their capital requires functioning payment systems, tariff stability, and credible off-taker arrangements. Zafiri’s $300 million first phase, which has mobilised $1 billion in total, is structured on the same conditions. Where those conditions hold, private capital follows concessional capital. Where they do not, it waits.

What This Means for Mission 300

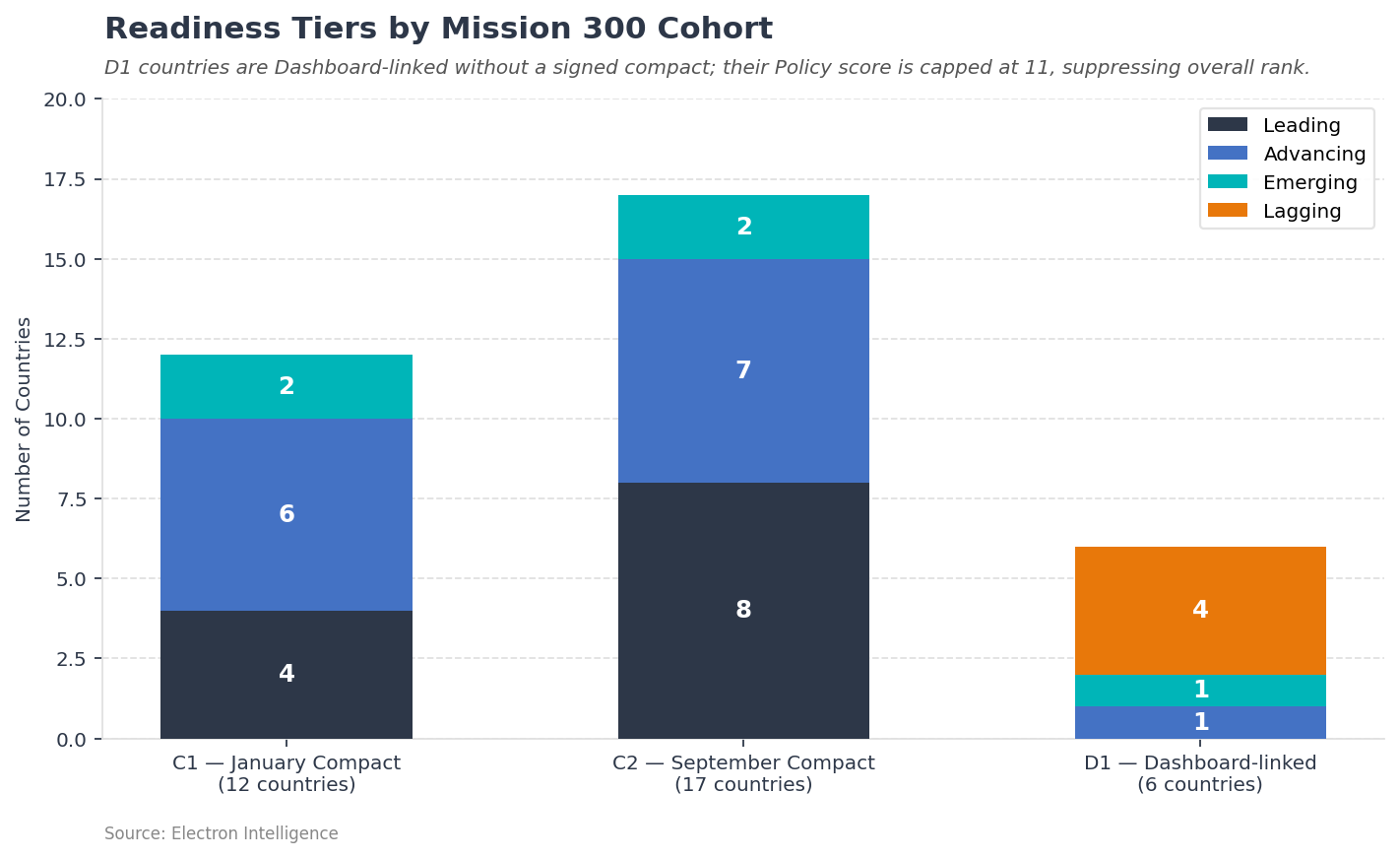

Exhibit 4: Tier distribution and delivery risk. The Leading tier holds enough capacity to push the 300 million target; whether the base broadens or narrows will determine if the programme succeeds on its own terms.

Mission 300 has generated visibility, alignment, and financing at scale. The 44 million connections delivered in the first fifteen months show that the platform moves capital. The remaining 256 million require institutional reform at pace.

For governments, target-setting and institutional capability need to be planned together. For the World Bank, AfDB, and their concessional partners, institutional support to the D1 cohort and to the ambition-heavy, foundation-light group produces more delivery leverage per dollar than incremental capital to the Leading tier. For the Private Sector Council and its member companies, execution risk sits in the underlying system. Compact signatures do not move that system.

No model predicts which countries will deliver the most connections by 2030. What the data establishes is where institutional gaps are wide enough to stall a $10 billion programme. For the 23 countries below the Leading tier, the next 12 months will test whether compact signatures translate into regulatory upgrades, utility reform, and procurement discipline. That sequence will shape Mission 300’s outcome more than any additional capital commitment.