The decisive institution in African power-sector reform is the electricity regulator, and the regulators in question operate very differently across markets. The Egyptian regulator has raised the residential electricity tariff multiple times since 2022, each move under International Monetary Fund (IMF) Extended Fund Facility conditionality. Ghana’s regulator publishes a tariff review on a 90-day cycle. Cameroon’s regulator has not moved a base tariff in thirteen years. The same nominal institution operates very differently across African markets, and the IMF, the World Bank, and the African Development Bank (AfDB) have begun writing that variation into the disbursement schedules of power-sector reform programmes, anchoring conditionality on tariff trajectories the regulator must publish rather than on balance-sheet outcomes the utility must deliver.

This audit covers what the regulators are doing. Across fifteen major African utility offtakers, only two regulators set a tariff that covers the cost of supply. The other thirteen do not, and the failure mode varies. Where the regulator can operate the tariff as a working mechanism, independent power producer (IPP) capital can underwrite against it. Where the regulator cannot, the bankability question reorients to the sovereign’s willingness to absorb the cost-recovery gap on the fiscal balance. Two of fifteen pass the first test. Three ring-fenced sovereigns (South Africa, Egypt, Morocco) pass the second. The other ten markets sit between.

Executive Summary

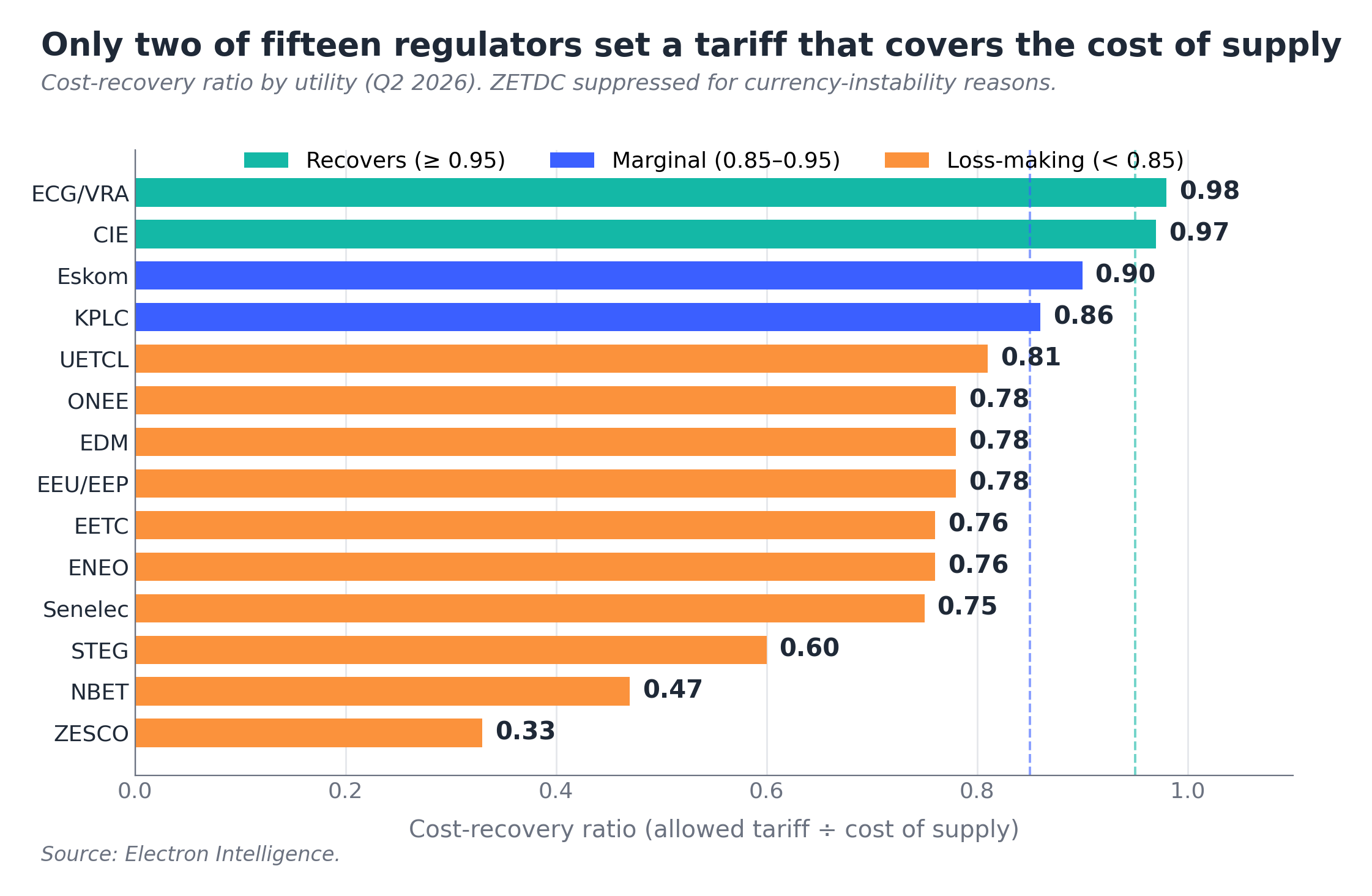

- Two of fifteen cover cost. Ghana’s ECG/VRA at 0.98 and Côte d’Ivoire’s CIE at 0.97. Eskom sits marginal at 0.90. The other twelve are below the recovery line, and the failure mode varies.

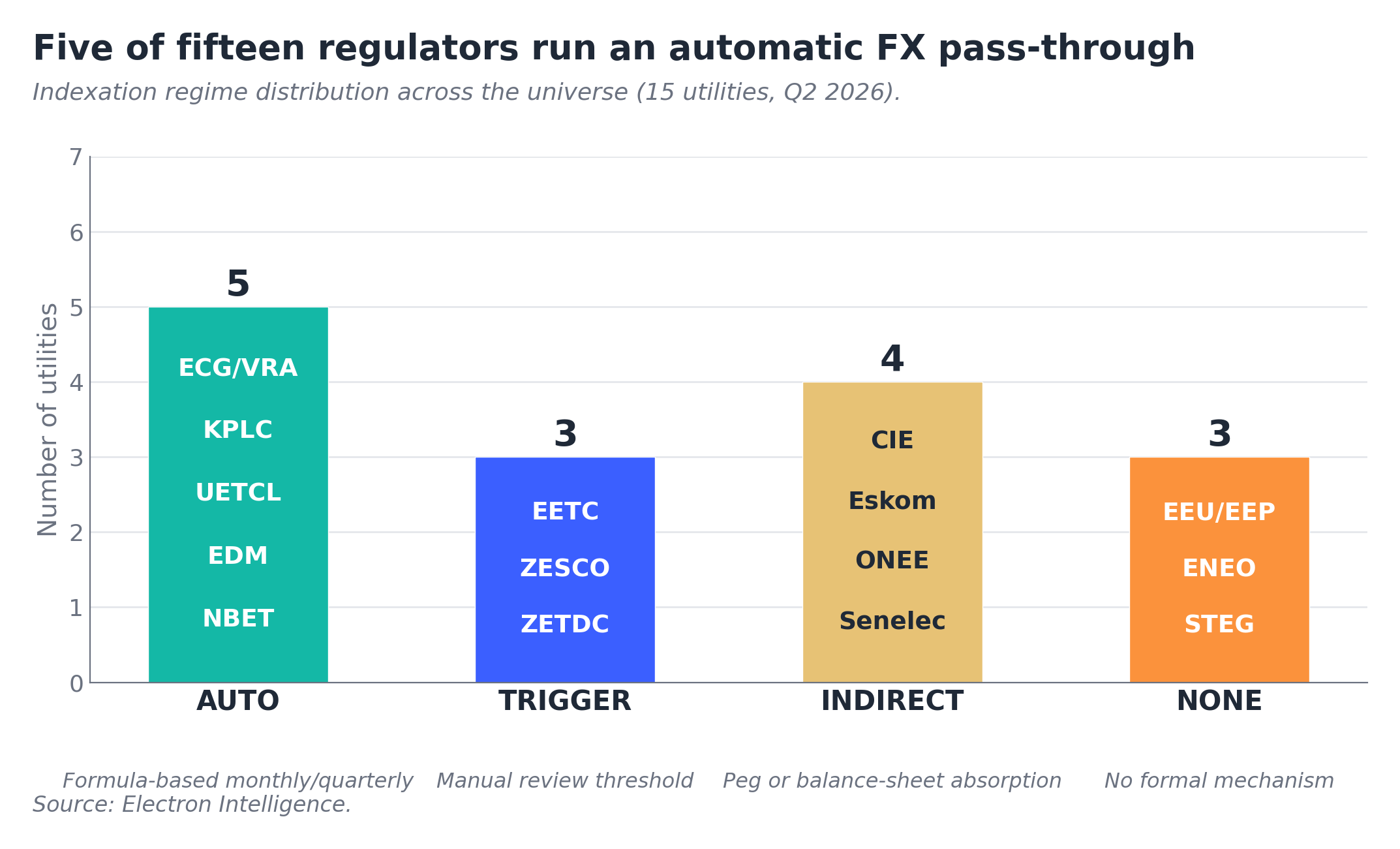

- The mechanism has four levers. Methodology family, review cadence, FX indexation, political pass-through. Five regulators run all four functionally. Ten cannot.

- The failure modes are distinct, not a single problem. Mechanism live but FX uncovered (KPLC, ZESCO, NBET, EDM). Mechanism suspended by decree or cabinet (STEG, ENEO, EEU/EEP). Mechanism opaque to outside readers (EDM, Senelec, CIE, UETCL). Each requires a different policy fix.

- Tariff cost-recovery and IPP bankability are separable. South Africa’s Eskom 0.90, Egypt’s EETC 0.76, Morocco’s ONEE 0.78. All three are loss-making at the tariff but bankable at the IPP level because the sovereign has absorbed the cost-recovery gap onto the fiscal balance.

- The underwriter’s question is institutional. Whether the regulator can operate the mechanism, not what number the tariff prints, determines forward bankability.

The Reference Case: When the Mechanism Works

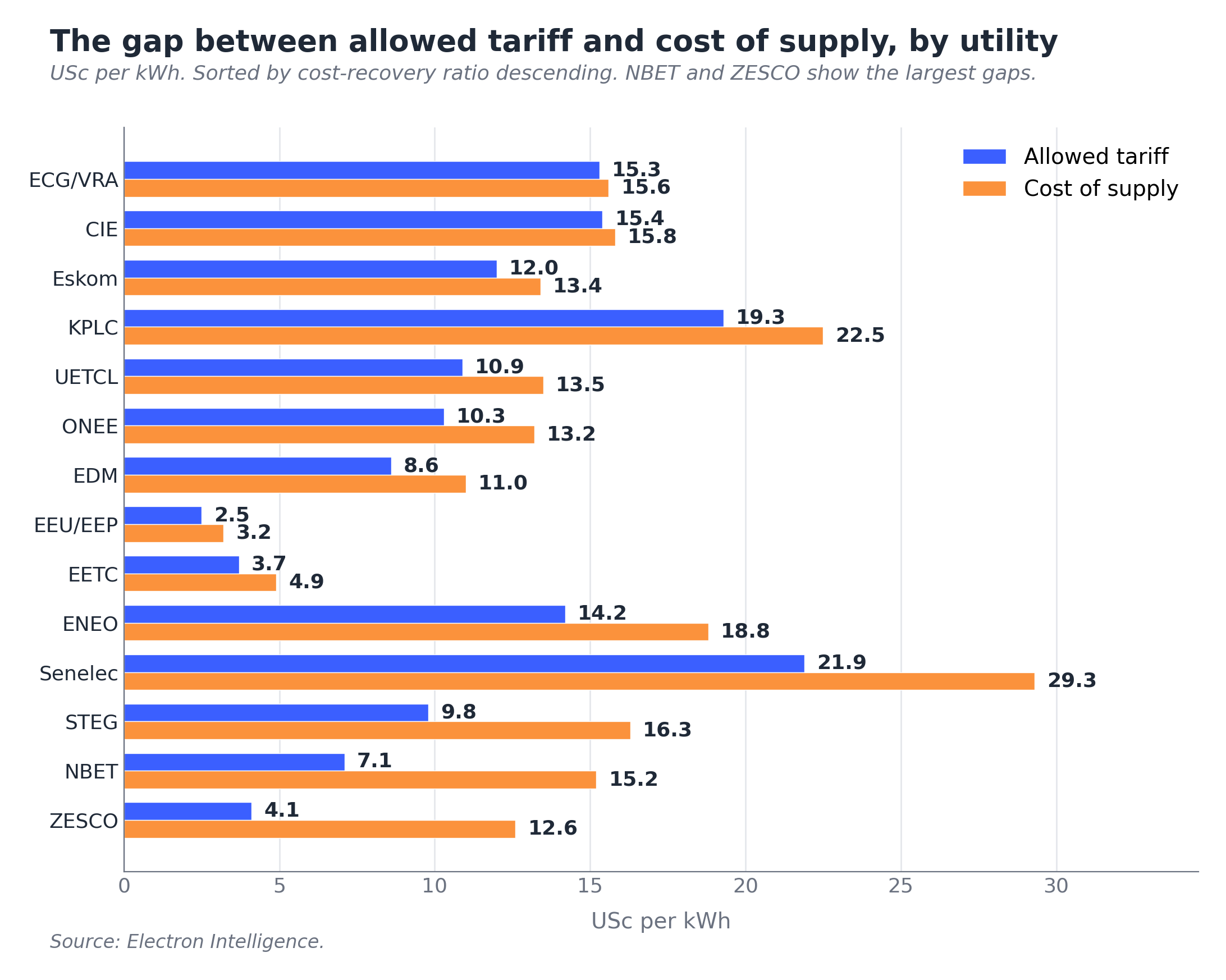

Kenya’s tariff does what a tariff is meant to do. When the shilling weakens, the bill rises within thirty days. When the shilling holds, the bill holds. The Kenya Power and Lighting Company (KPLC) cost-recovery ratio prints at 0.86, with allowed tariff of 19.3 US cents per kilowatt-hour against cost of supply of 22.5, and the 14% gap closes mechanically every month as the indexation formula fires.

Three institutional features hold the mechanism together. Kenya’s Energy and Petroleum Regulatory Authority, EPRA, sets a multi-year base tariff under a cost-plus formula reviewed every three years. A monthly gazette notice, the Foreign Exchange Rate Fluctuation Adjustment, passes USD-denominated supply contract costs through to retail at the prevailing exchange rate. EPRA is statutorily independent under the Energy Act 2019, and its orders are appealable in court rather than overrideable by cabinet decree.

That combination of live methodology, short review cycle, automatic monthly indexation, and statutory independence is what makes a tariff regulator functional. Where any of the four breaks in the other markets, the failure produces a distinct pattern.

Figure 1: Cost-recovery ratio across fifteen African utility offtakers, Q2 2026.

Three Ways the Mechanism Fails

Failure mode one: mechanism live, FX uncovered

The most common failure pattern is a working methodology with a broken indexation lever. The regulator sets a tariff, the review cycle is regular, the orders are public, but the FX adjustment formula either lags the market or is absent entirely.

Ghana’s Public Utilities Regulatory Commission (PURC) runs a quarterly tariff review formula that references the dollar-to-cedi rate against a base set in each tariff order. The mechanism is live. ECG/VRA’s cost-recovery ratio at 0.98 is the highest in the universe. But the 0.98 print is partly the result of the cedi rally through Q1 2026, from 14.6 to 10.79 against the dollar. A cedi reversal restores the gap because the regulator can only re-index at the next 90-day boundary.

Nigeria’s Multi-Year Tariff Order (MYTO) 2024 includes a Band A 220% tariff hike and a partial FX pass-through trigger via biannual minor reviews. The mechanism is live but the indexation is sticky. Nigerian Bulk Electricity Trader (NBET) prints a 0.47 cost-recovery ratio because the cost-reflective tariff sits at 15.2 US cents while the allowed average across all bands sits at 7.1. The Federal Government’s subsidy bridges the gap. Extension of Band A pricing logic to Bands B and C is the only credible path to a measurable cost-recovery improvement at NBET, and the timing is political rather than regulatory.

Zambia’s Energy Regulation Board (ERB) operates a multi-year tariff framework with a quarterly review trigger if the kwacha moves more than 10% against the dollar. The threshold is not formally published in the ERB order, which makes the mechanism a manual review in practice. ZESCO prints a cost-recovery ratio of 0.33, and the print reflects what the regulator filed, not what an automatic formula would produce.

Figure 2: Allowed tariff against cost of supply, USc per kWh, by utility, Q2 2026.

Failure mode two: mechanism suspended

In a second cluster, the mechanism does not exist in operating form. The regulator either does not have current authority to set a tariff, or has not exercised it for so long that the methodology is effectively superseded by cabinet decree.

Cameroon’s national utility, ENEO, operates under a base tariff frozen since May 2012 by the country’s electricity regulator (ARSEL). The tariff has not moved in thirteen years. The November 2025 prepaid-postpaid alignment was a billing-system reform, not a tariff revision. ARSEL exists as an institution but is not currently operating the tariff-setting lever. A post-renationalisation review is pending in Q3 2026.

Tunisia’s national utility, STEG, operates under cabinet decree rather than a methodology-driven regulator. Tariff increases happen on ad-hoc dates determined by Council of Ministers decision (2022, 2023, 2025). The state compensation fund absorbs the difference between cost and tariff, at roughly 5% of gross domestic product per IMF estimates. STEG’s cost-recovery ratio of 0.60 is what cabinet has chosen to set, not what an independent regulator would determine.

Ethiopia’s national power utilities, EEU and EEP, operated under a phased multi-year tariff roadmap that was effectively halted by the August 2024 birr devaluation. The Ethiopian Energy Authority was reorganised in 2024 and the Ministry of Water and Energy retains de facto override. A new tariff order is expected in Q3 2026 once the birr stabilises. Until it lands, the mechanism is suspended in the same way Cameroon’s is.

Failure mode three: mechanism opaque

The third failure pattern is opacity. The methodology may exist, the review cycle may run, the indexation lever may even be active, but the regulator publishes too little for outside readers to verify which levers are doing what.

Mozambique’s Electricidade de Moçambique (EDM), Senegal’s Senelec, Côte d’Ivoire’s CIE, and Uganda Electricity Transmission Company Limited (UETCL) all sit here. Methodology family and review cadence are publishable. The cost-of-service determination that the cost-recovery ratio depends on requires inference from World Bank Public Expenditure Reviews, IMF Article IV reports, and African Development Bank (AfDB) sector studies. These utilities are not unbankable. They are just unauditable from public regulator filings alone.

Figure 3: Indexation regime distribution across fifteen utilities, Q2 2026.

Where the Pattern Breaks

Two utilities sit outside the three failure modes for different reasons.

Zimbabwe’s Zimbabwe Electricity Transmission and Distribution Company (ZETDC) is a currency story rather than a regulator story. The Zimbabwe Energy Regulatory Authority (ZERA) publishes tariffs, but the Zimbabwean Dollar (ZWL) to Zimbabwe Gold (ZiG) transition has made any local-currency tariff figure unreliable for USD comparison. The cost-recovery ratio cannot be computed at primary-source quality, regardless of what ZERA prints. ZETDC is the universe’s only fully opaque entry.

Côte d’Ivoire’s CIE prints the universe’s second-highest cost-recovery ratio at 0.97, but the print reflects the currency peg as much as the regulator. The Communauté Financière Africaine (CFA) franc zone fixes the local currency to the euro at 655.957 to 1, removing most FX risk from the tariff stack. The Eranove concession contract sets the cost-plus structure on advice from the Autorité Nationale de Régulation but the Council of Ministers approves the final schedule. CIE is at 0.97 not because the regulator is doing something different from the others but because the currency lever is muted before any tariff decision is made.

The Separation Finding

The headline finding from the audit is that tariff cost-recovery and IPP bankability are separable variables. They are not different framings of the same question. They measure different things and can move independently.

Three ring-fenced utilities prove the separation directly. South Africa’s Eskom prints a cost-recovery ratio of 0.90. Egypt’s national grid operator, EETC, prints 0.76. Morocco’s national power utility, ONEE, prints 0.78. All three are below the recovery line and loss-making at the tariff level. Yet all three operate IPP payment structures that are insulated from utility distress through sovereign back-stop mechanisms operating independently of the tariff.

For Eskom, the back-stop runs through National Treasury equity injections (the R350 billion programme) plus the R254 billion Debt Relief Act of 2023. For EETC, it runs through Ministry of Finance subsidy transfers (EGP 154 billion in the FY 2024/25 budget) and Central Bank FX availability priority for IPP dollar obligations under the IMF Extended Fund Facility (EFF). For ONEE, it runs through the state guarantee on ONEE debt (Loi 40-09) and Treasury counter-guarantees on AfDB and World Bank loans, with the sovereign’s investment-grade rating providing market access.

The mechanism in each case is the same. The sovereign relocates the cost-recovery gap from the utility’s payables to the fiscal balance. The tariff stays below cost. The IPP gets paid on schedule. The shortfall is borne openly by the Treasury rather than accumulated covertly against the supplier. The audit’s finding for forward IPP capital is this: not whether the tariff covers cost, but whether the sovereign bears the gap openly enough to make IPP cash flows predictable.

What We’re Watching

Three near-term events will move three utilities between failure modes before Q3 2026. Cameroon’s electricity regulator (ARSEL) will conduct a post-renationalisation tariff review that determines whether the frozen base tariff finally moves and whether ARSEL re-establishes a publishable methodology. Ethiopia’s Ethiopian Energy Authority is expected to issue a new tariff order once the birr stabilises and the IMF Special Drawing Rights programme conditionality binds. Tunisia’s STEG remains conditional on revival of the IMF programme; without it, its publishable disclosure level holds only as long as supplier-payables disclosure continues.

Separately, the ZESCO cost-of-service reconciliation closes before the next quarterly update. The 12.6 US cent cost figure may include drought-period thermal imports averaged into the determination, in which case the audit will distinguish normalised and realised cost-recovery as a methodological refinement.

Bottom Line

Where the regulator can operate the mechanism, with methodology live, indexation automatic, and institutional independence intact, capital can underwrite against the tariff. Where the regulator cannot, the IPP underwriting question reorients to the sovereign’s willingness and capacity to absorb the cost-recovery gap on the fiscal balance.

Two regulators in the universe run the mechanism functionally. Three sovereigns have internalised the gap and substituted their own credit for the tariff. The other ten markets sit between, where a forward IPP contract requires either a regulator-strengthening trajectory that the underwriter has to believe in or a guarantee structure that converts the tariff risk into sovereign exposure.