Executive Summary:

- Nigerian DisCos recorded better commercial performance in 2024, with improvements in both billing efficiency and collection efficiency. The gains were material, but not enough to restore commercial stability across the market.

- Billing improved but remained incomplete. Nigerian DisCos recorded a billing efficiency of 82% in 2024, meaning 5,206.59 GWh of received energy was not billed.

- Cash conversion remained weak. Nigerian DisCos recorded a collection efficiency of 56% in 2024, leaving more USD 361 million (₦536 billion) of billed revenue uncollected.

- The electricity sector continued to lose value at two critical points: before delivered energy became billed consumption, and after billed revenue was expected to become cash.

- Weak billing and collections continue to affect market settlements, generation payments, gas supply obligations, and the broader fiscal burden required to keep the system functioning.

- Higher billed values alone do not solve the problem. Improving collection discipline matters more than tariff increases. Without stronger collections, higher tariffs will simply widen the absolute value of uncollected revenue.

- The overall picture is one of improvement without resolution: a more disciplined market than before, but still some distance from the revenue stability needed for durable power sector recovery.

The first full year under the 2023 Electricity Act has offered the clearest view yet of the commercial state of Nigeria’s distribution market. On paper, 2024 was stronger than the two years before it. DisCos converted a larger share of delivered energy into bills and a larger share of those bills into cash. This improvement matters because distribution remains the main cash recovery point for the wider power market.

On the national average, billing and collection efficiencies improved in 2024, but not enough to close the commercial gap. Nearly 18% of delivered energy did not become billed consumption, and more than USD 361 million (₦536 billion) in billed revenue remained uncollected. In other words, the market is still losing value at two critical points: before energy becomes revenue, and after revenue has already been booked. That is why stronger collections, on their own, were not enough to restore commercial stability.

The Market Is Not Failing in One Uniform Way

The first important distinction is between billing-led weakness and collection-led weakness. A DisCo can convert a reasonable share of energy into bills and still collect poorly. Another can collect reasonably well on the bills it issues, but still fails to capture a sufficient share of delivered energy in the billing system in the first place. Those are different commercial problems, and they require different operational responses.

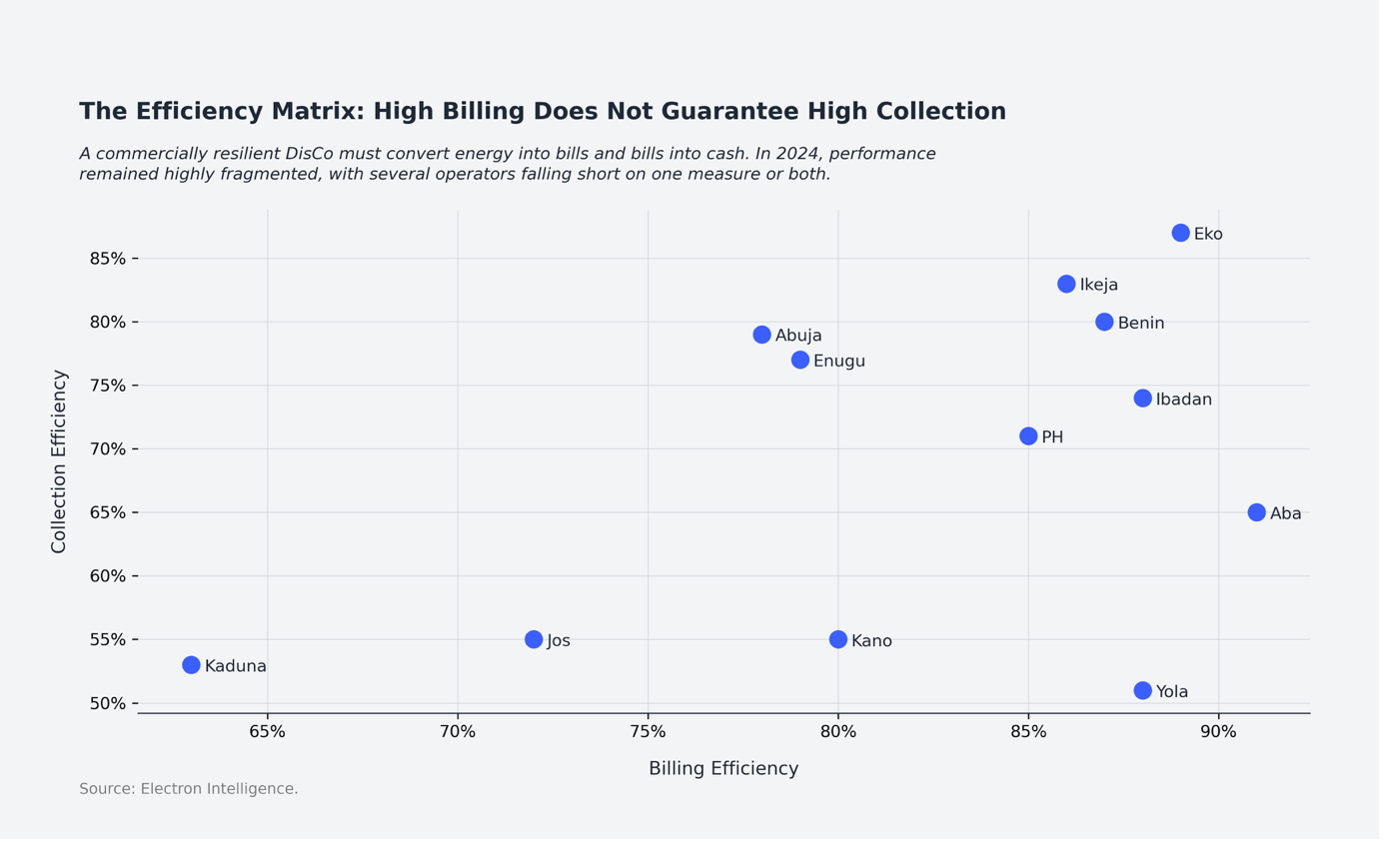

The scatter plot above shows that stronger billing does not automatically translate into stronger collections. Several DisCos sit relatively far to the right, meaning they convert a large share of delivered energy into bills, but still sit lower on the collection axis, showing that cash recovery remains weak even after revenue has been booked. Others sit weakly on both axes, with poor billing conversion compounded by weak collections. A simple segmentation of 2024 performance reinforces the point. Some operators, such as Eko and Benin, appear more collection-constrained, while others, such as Abuja and Ikeja, show a more mixed pattern. Several weaker-performing DisCos remain constrained on both fronts. The implication is that the primary leakage point differs across utilities: some are mainly billing-constrained, others are more collection-constrained, and several remain weak on both fronts.

A commercially resilient DisCo must perform well on both measures at the same time: it must convert delivered energy into bills, and those bills into cash. In 2024, too many operators were still falling short on one side or both.

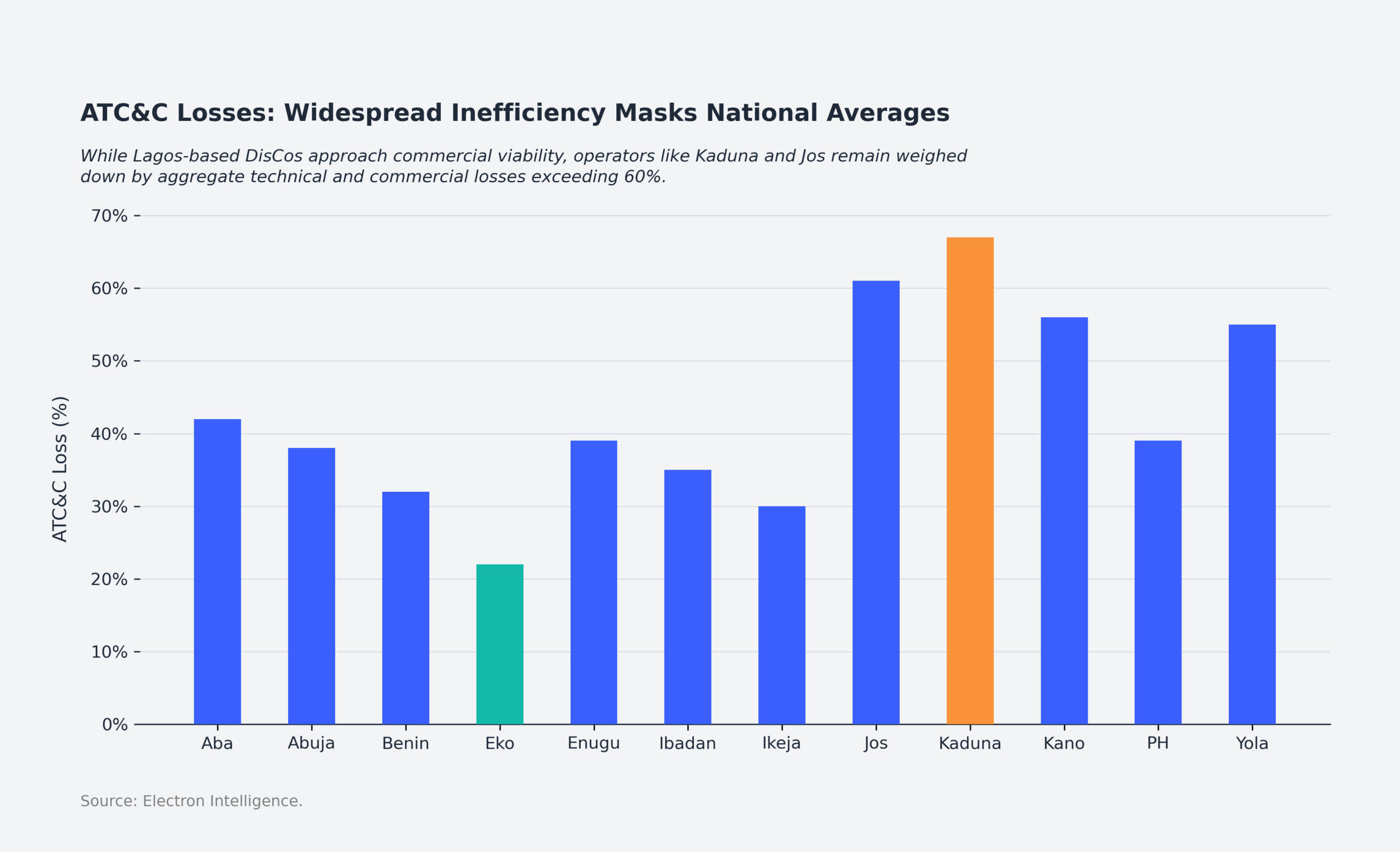

While the scatter plot shows where the primary leakage sits across utilities, the Aggregate Technical and Commercial (ATC&C) losses chart strengthens that point by showing how widely total losses still vary across the market. National averages suggest improvement, but they mask a wide performance spread across DisCos. Some operators, especially in Lagos, are closer to stronger commercial performance, while others, such as Jos, Kaduna, and Kano, remain weighed down by very high aggregate technical, commercial, and collection losses. The implication is that there is no single national commercial problem. Rather, there is a collection of regional and operational breakdowns sitting beneath one headline number.

Metering and Billing Integrity Still Matter

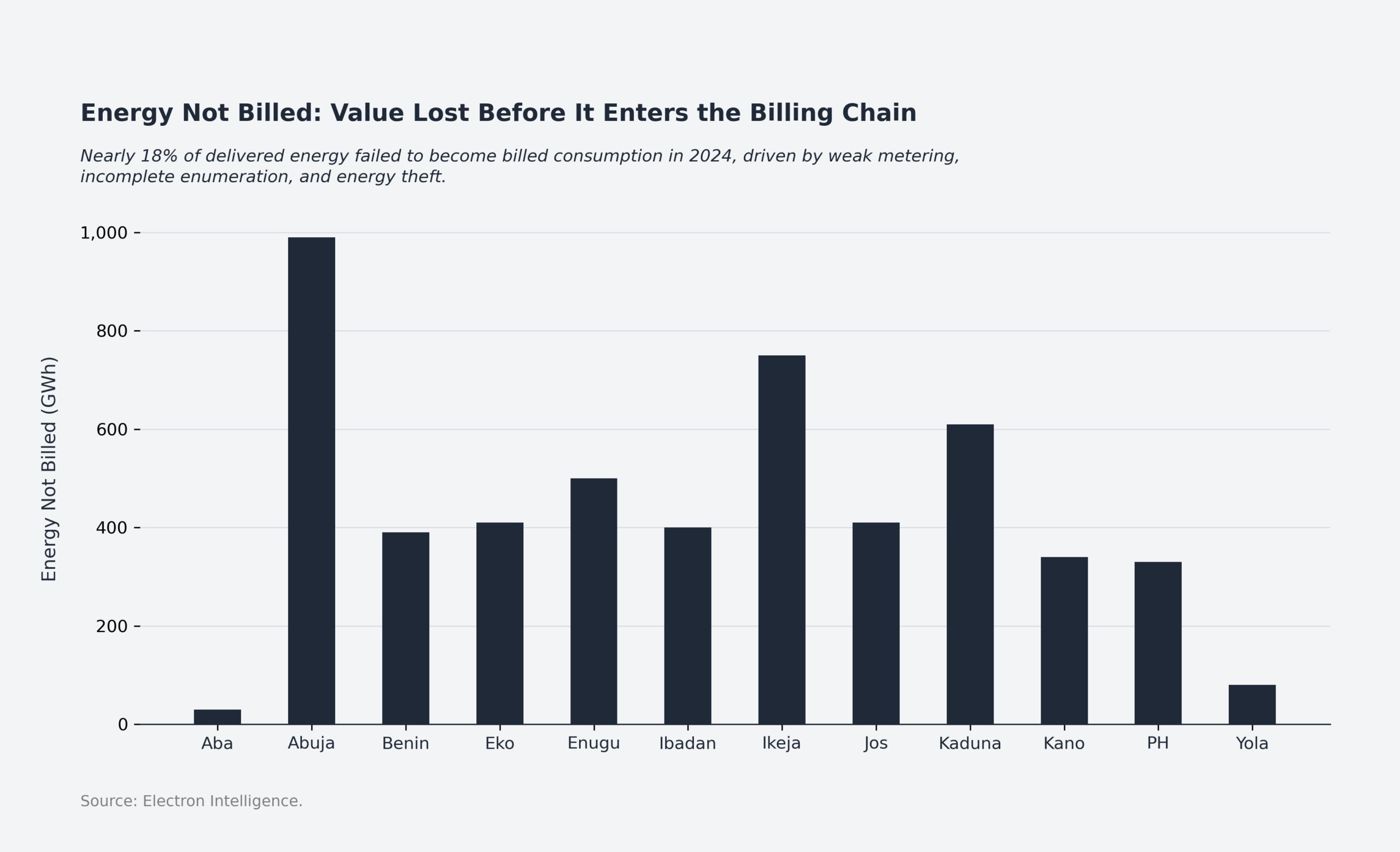

The energy-not-billed chart shows that the first commercial leakage often occurs before collections even begin. Several DisCos still record a large gap between energy received and energy billed, but the burden is not evenly spread. Abuja is the clearest outlier, with a much larger stock of unbilled energy than the rest of the market, while Ikeja and Kaduna also remain notably elevated. By contrast, Aba and Yola sit at the lower end of the distribution. The pattern shows that in some service areas, a far larger share of delivered electricity is failing to enter the billing chain at all. In those markets, weak metering, incomplete customer visibility, poor feeder-level accounting, and theft are likely playing a larger role.

The Liquidity Problem Did Not Go Away

The USD 361 million (₦536 billion) gap between billed revenue and collected revenue explains much of the market’s continuing strain. The issue is not only that tariffs have historically been below cost-reflective levels. It is also that even billed revenue does not fully convert into cash. Since distribution is the main cash recovery point in the value chain, weak collections do not stop at the customer interface. They move upstream through market settlements, generation payments, gas supply obligations, and ultimately the fiscal burden required to keep the system functioning.

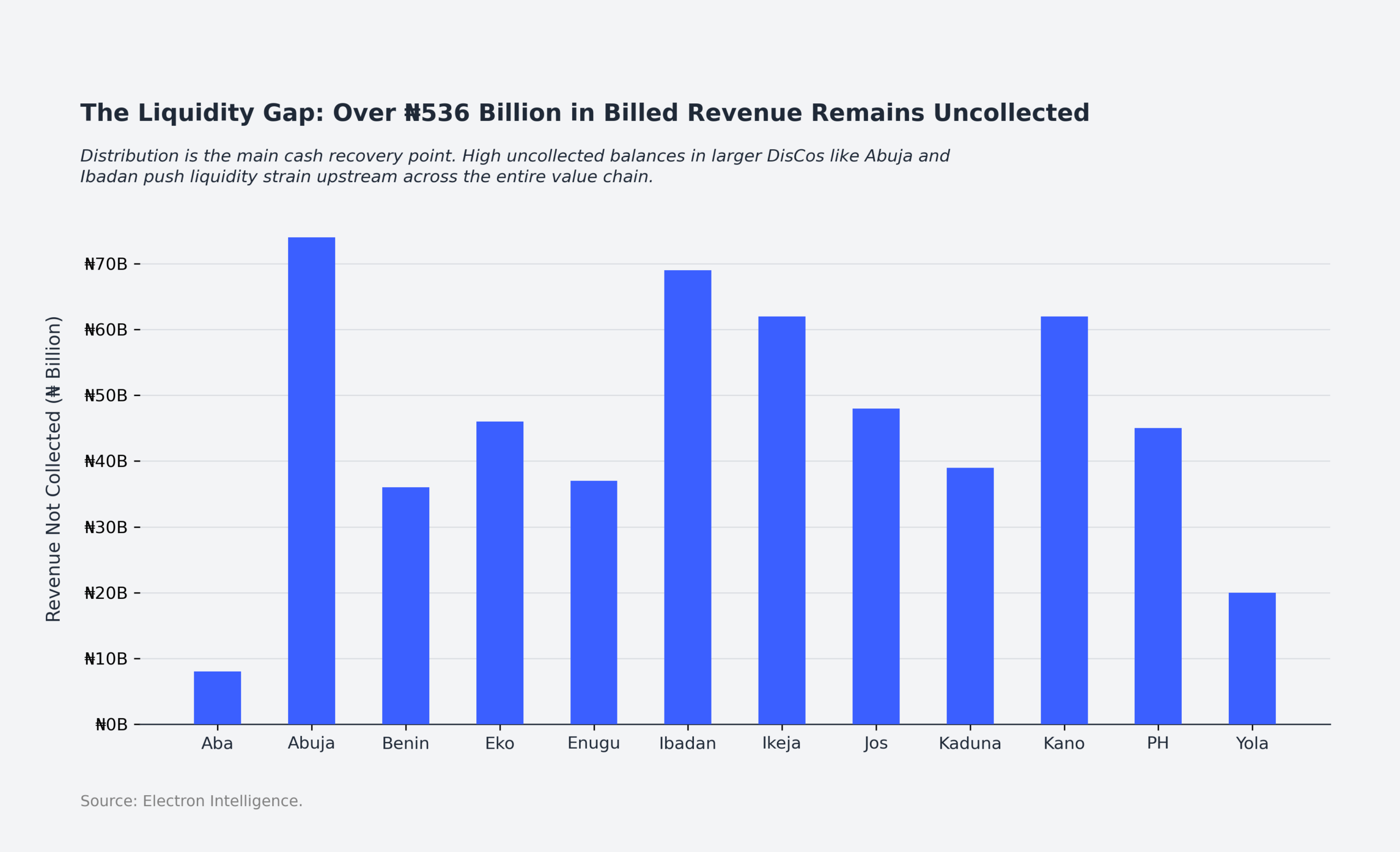

The revenue-not-collected chart shows that this burden is concentrated rather than evenly spread. Some of the largest unpaid balances sit with the bigger billing utilities, meaning that even moderate weakness in collection efficiency can translate into very large cash shortfalls in absolute terms. Those outliers matter because they show how a few large DisCos can account for a disproportionate share of revenue left uncollected. A utility can post high billings and still deepen market stress if too much of that billed value never becomes cash. It also shows why the sector’s commercial challenge cannot be explained by tariffs alone. Higher tariffs may raise the value of bills issued, but if collection discipline does not improve, the market simply carries a larger stock of unpaid revenue.

The Commercial Gap: Why Efficiency is Not Liquidity

The central problem in the Nigerian power market is that marginal efficiency gains are not enough to repair a weak cash cycle. In practice, the DisCo remains the cash collection point for the wider system. When revenue is not collected at the distribution end, the shortfall does not stay there. It flows backward across the value chain: bulk trading obligations weaken, generation payments fall short, gas suppliers face delayed settlement, and public intervention continues to fill part of the gap. That is why better commercial ratios, while important, still fall short of restoring market liquidity.

Where Commercial Recovery Must Begin

The commercial problem facing DisCos is not simply that efficiency remains too low. It is that revenue control remains weak. More energy is being billed, and more revenue is being collected, but not yet at a level that materially improves market liquidity. That is why the next phase of reform should focus less on aggregate national targets and more on where value is still being lost within each utility.

DisCos must tighten feeder-level energy accounting. The first commercial gap in many service areas is not collections but visibility. Energy is delivered, but part of it never enters the billing chain cleanly because feeder performance, customer connections, commercial losses, and technical losses are still not tracked with enough precision. Without that visibility, utilities cannot isolate where value is being lost or improve billing quality in a durable way.

DisCos must reduce unbilled energy before pursuing higher billed revenue. A utility that expands billed value without first addressing the share of energy that never reaches the billing system risks deepening its own inefficiency. In several markets, the more immediate issue is not low tariff application but weak conversion of delivered energy into billable consumption. Customer enumeration, meter integrity, connection regularisation, and better loss measurement need more attention if billing efficiency is to improve durably.

DisCos need to retain higher-paying demand more deliberately. In many service areas, higher-paying customers are increasingly relying on self-generation, selective grid offtake, or backup arrangements rather than full dependence on the network. That weakens the customer segments that would normally provide more stable cash generation. Service improvement, especially in areas with dense and creditworthy demand, should therefore be treated not only as a technical goal but as a commercial priority.

State regulators and state governments must use their authority to strengthen payment discipline. In weaker markets, poor collections often reflect more than customer affordability. They also reflect weak enforcement, unresolved public-sector arrears, and limited consequences for persistent non-payment. The bigger challenge is that many state markets remain transitional in practice, with parts of the new framework still relying on inherited federal structures and implementation processes rather than fully active state-level regulation. Where states now have regulatory standing, the practical test will be whether they can move beyond that inheritance, improve enforcement, compel public-agency compliance, and create a more credible collections environment for utilities and investors.

The Bottom Line: Where the Market Stands

The first full year after the Electricity Act points to a better commercial year for Nigeria’s DisCos. Billing improved, collections improved, and cash recovery strengthened. But the market still fell short of commercial stability. Revenue leakage remains significant, performance remains uneven across utilities, and the wider value chain still relies on support beyond what normal market collections can sustain. The result is improvement without resolution: a more disciplined market than before, but still far from the revenue stability needed for durable sector recovery.