A Landed Cost Breakdown of Solar in Nigeria and What Sets the Price

Imported modules and inverters reach a Nigerian developer site at $0.16 per watt, 14 percent over the factory price, and none of it is import duty or value-added tax. This analysis builds the delivered cost line by line and shows that the number is set by the equipment and the currency, and that it rests on a single duty and VAT exemption.

A 20 megawatt (MW) project sources its modules and inverters from China, ships them to Lagos, clears customs, and trucks them to the site. None of those steps is where the cost is. Solar equipment enters Nigeria at a zero tariff, free of both import duty and value-added tax, so the border adds almost nothing. If the cost is not at the border, it sits in the equipment and in the currency behind it, both set well outside Nigeria. This piece follows the cost from the factory to the site and shows what actually sets it: the module price, the exchange rate, and one duty-and-VAT exemption that behaves less like a tax rule than a switch.

Executive summary

- The delivered cost is low, and it is not about tariffs. Imported solar equipment lands in Nigeria at 14 percent over the factory price. That premium is driven by the equipment and the currency, not the border.

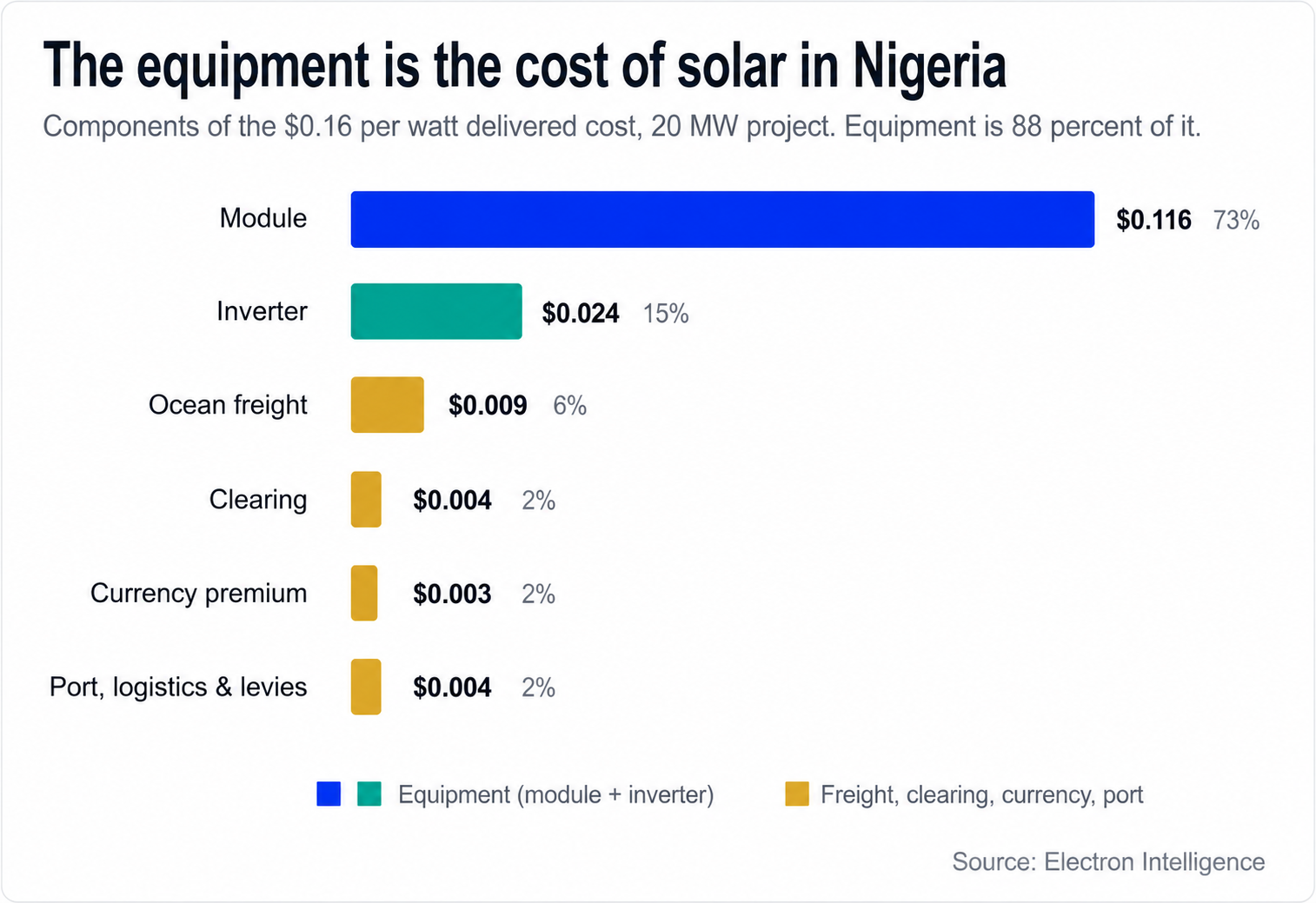

- The equipment is almost the whole bill. The module is 73 percent of the delivered cost and the inverter 15 percent, leaving freight, clearing and haulage a thin layer on top. A swing in the module price moves the delivered cost fifteen times as much as an equal swing in freight.

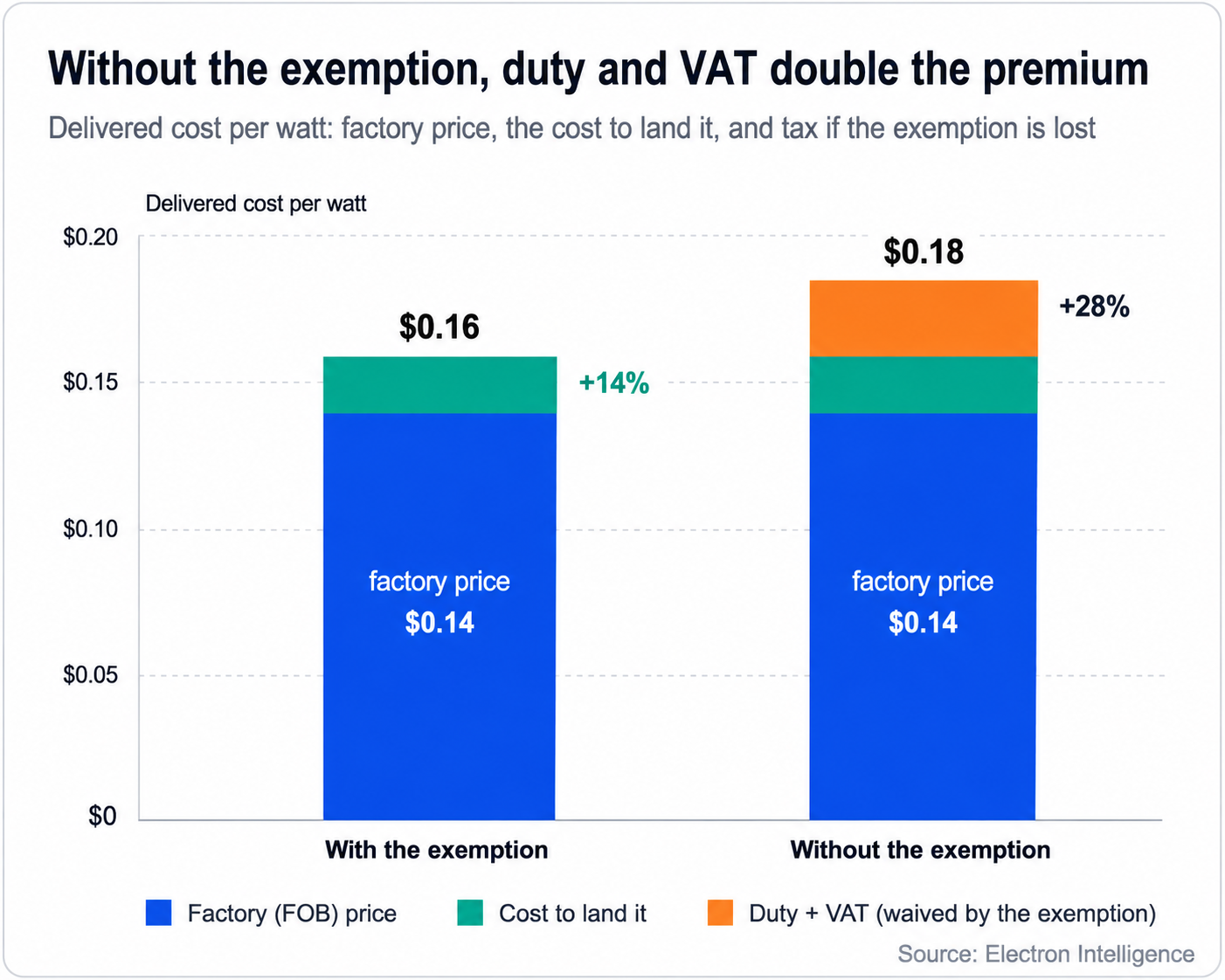

- The low premium rests on one exemption. Solar equipment enters free of duty and value-added tax, a relief worth $0.02 per watt. If it lapses, whether by policy or by a classification challenge at the customs desk, the full statutory charges return and the premium over the factory price doubles.

- The biggest driver of the price is set in China: the module is the largest part of the bill, and its price is set in the Chinese market. China's removal of its 9 percent solar export rebate in April 2026 lifted factory prices by about that amount directly, with the rest of the increase driven by a roughly 30 percent spike in silver costs and tighter manufacturer supply discipline, and that fed straight into the Nigerian delivered cost.

- Where it goes next. The module's forward price curve is flat to softening into late 2026, which pulls the delivered cost down. Pushing the other way: the return of a suspended 4 percent import levy, or a ruling on the proposed import ban. The panel price and policy will decide what happens next.

Imported modules and inverters land at 14 percent over the factory price, with no import duty or VAT to pay

Nigeria is now the second-largest importer of solar modules in Africa, behind only South Africa, at roughly 1.7 gigawatts in the year to mid-2025. Most of that went into off-grid and commercial-and-industrial (C&I) systems, which account for almost all of Nigeria's installed solar capacity. Whatever the end use, the equipment moves through the same supply chain, and a 20 MW project is a clean unit to price.

For a 20 MW project, modules and inverters arrive on site at $0.16 per watt, compared with a factory price of $0.14. That factory figure is what the trade calls free-on-board, or FOB: loaded onto the ship with export clearance done, nothing beyond that paid. The 14 percent gap is everything it takes to move the equipment from a Chinese port to a Nigerian site and clear customs.

For most imported goods, that gap would be much wider because duty and value-added tax would fall within it. Solar equipment is treated differently. Correctly classified, modules and inverters enter Nigeria at zero import duty and are exempt from the 7.5 percent value-added tax. Two things secure that: a customs ruling that files them under tariff heading 8541 (the code for photovoltaic cells and modules), and a 2025 tax law that preserves the relief.

One statutory charge does survive. The ECOWAS Community Levy, a half-percent charge the West African bloc applies to goods from outside the region, is due whether or not import duty is. Here, it comes to a fraction of one percent of the delivered cost. Once duty and value-added tax fall away, very little is left on the statutory side.

The module price sets the delivered cost, and the exchange rate moves it next

The cost is in the equipment. The module is 73 percent of the delivered total and the inverter 15 percent, together 88 percent of the bill, a share of landed equipment cost, not of total installed project capex, where the module runs closer to 18 percent. Nothing else on it is large.

The remaining 12 percent is spread thin across ocean freight (the largest slice), clearing and bank charges, the premium to buy dollars, and port handling and haulage. No single one of them would move the delivered cost in a way a budget would notice. Figure 1 shows the full build.

What moves the delivered cost is the module price. Across the $0.10 to $0.14 per watt a buyer might be quoted, the delivered cost shifts by $0.04, fifteen times what an equal swing in freight does. Freight is the larger cost, but the exchange rate is the larger risk: the premium to buy dollars can widen from 1 to 5 percent when they are scarce, and that swing moves the delivered cost more than freight ever would. The panel price and the exchange rate matter most, in that order, and both sit well above anything at the port.

Figure 1. Where the cost sits: the delivered cost built up from the factory price. The module is 73 percent of the bill and the inverter 15 percent; freight, currency, clearing and the rest are thin slices, and the tax line is zero.

The low premium rests on one duty and VAT exemption, and that exemption behaves like a switch

The 14 percent premium holds only as long as the exemption does. The relief is worth $0.02 per watt, the whole of what freight, clearing, currency and logistics add together.

With the exemption in place, the delivered cost sits 14 percent over the factory price. With it gone, a 5 percent import duty and 7.5 percent value-added tax return, and the premium doubles. There is no middle setting: a project either holds the relief or it does not.

The exemption can be lost two ways. The first is policy. The government could withdraw the relief or let it lapse. The second is administrative, and more immediate: the zero rate depends on the equipment being entered under the correct tariff heading, and Nigerian customs officers have in the past filed solar modules under a heading that carries duty. A single decision at the desk can move a project from the exempt case to the dutiable one, whatever the statute says.

Figure 2. The switch: delivered cost with the exemption on versus off. The relief holds the cost 14 percent over the factory price; removed, the statutory stack doubles it.

China's withdrawal of its solar export rebate in April 2026 raised the module price that dominates the bill

The largest single influence on what a Nigerian project pays for its modules is not a Nigerian decision at all. Chinese module prices had fallen to $0.08 per watt in 2024 and early 2025, the bottom of a deep oversupply.

Then, in April 2026, China's finance ministry removed the 9 percent value-added tax rebate it had granted to solar exporters, part of a wider effort to stop its manufacturers selling below cost. Chinese makers had built that rebate into their export prices, so removing it passed roughly 9 percent of cost straight to foreign buyers; the rest of the increase reflects a roughly 30 percent spike in silver costs and tighter manufacturer supply discipline. The module now sits at $0.116 per watt, well above the $0.08 floor of a year earlier.

Because the module is the bulk of a Nigerian project's delivered cost, a shift in Chinese export policy passes almost straight through to the Nigerian price, and this one already has.

Inside Nigeria, the risks to the exemption are an import ban, a recurring levy, and the VAT position

Three Nigerian policy lines are worth watching, and none of them is the ordinary tariff.

- A proposed import ban. Floated in 2025, it would bar solar panel imports outright to force local manufacturing. It is not in force in mid-2026, and it is a market-access question rather than a cost one, but it would change the picture entirely if enacted.

- A recurring 4 percent levy. This charge on the factory value of imports was switched on and off through 2025 and suspended again that September. Because it would apply to the FOB value regardless of the duty exemption, its return would reach solar even while import duty stays at zero.

- The VAT position itself. The 2025 tax law keeps solar exempt, now administered by a newly renamed revenue service. The relief holds until an official order changes it, and that order is the thing to watch.

What to check before you trust the number

Most of the delivered cost is outside anyone's hands on the ground: the module price is set in China, the exchange rate by Nigeria's currency market, the exemption by policy. The one line that turns on execution is whether the exemption is actually captured, and that is a paperwork question. Equipment entered under the correct 8541 heading clears at zero duty; a shipment an agent lets through under the wrong heading pays the full charge. For a developer it is the item to get right; for a lender or sponsor it is the diligence line that tells you whether the capex quote in front of you is the exempt number or the dutiable one. And the $0.16 per watt figure is itself a spot-priced, unfinanced floor — the cost of capital this piece excludes by scope is not a rounding line at Nigeria's 26.5 percent policy rate.

What we are watching

The module price, the dominant driver, is not fixed: its forward curve is flat to softening into late 2026, so the delivered cost could as easily drift down as up from here. The figure in this piece is a mid-2026 snapshot, to be re-taken whenever the module price moves.

A few smaller inputs are still estimates rather than firm quotes, among them the inverter's factory price and whether value-added tax on terminal handling is recoverable. None of them changes the shape of the finding, since the equipment and the currency dominate.

Above all, watch the exemption. The clearest signal would be the return of the 4 percent levy or a firm ruling on the import ban. Either would move the delivered cost off the number here.

Bottom line

The delivered cost of solar equipment in Nigeria is low today, 14 percent over the factory price. Waived duty and value-added tax explain that, while the ports themselves are ordinary. The cost is set by the equipment and the dollars required to buy it, both driven by decisions made outside Nigeria. From within Nigeria, the tariff rate is set at zero; the open question is whether the exemption underlying that zero rate survives. As long as it holds, the number stays put; if it lapses or a classification challenge overturns it, the premium doubles. The exemption is therefore the decisive variable, since the entire low premium depends on it.