The Wheeling Map: Where African Developers Can Sell Power Around the Utility, and at What Cost

South Africa's wheeled model delivers power at about $0.045/kWh (R0.73), roughly 60 percent below the $0.114/kWh (R1.85) utility tariff. This analysis maps the African markets where the power wheeling rail is built, half-built, or blocked, and prices the delivered cost in each.

South Africa's wheeled model delivers power at about $0.045/kWh (R0.73), roughly 60 percent below the $0.114/kWh (R1.85) utility tariff. This analysis maps the African markets where the power wheeling rail is built, half-built, or blocked, and prices the delivered cost in each.

South Africa has built what other African markets have only legislated. A developer generates power at a remote site, pays the utility a fee to move it across the existing grid, and sells it to an industrial buyer at about $0.045 per kilowatt-hour, roughly 60 percent below Eskom's tariff. For industrial buyers that cannot generate on their own land, wheeling has become the standard way to buy clean power.

Nine other markets have the same law on their books, but few have a working market to match: of the ten where wheeling is legal, only six publish a price, three carry any third-party power, and one carries it at scale. And even where the route is open, and the power is cheap, what usually gets a deal financed turns on something no wheeling tariff can touch: the country's currency, its solvency, or a congested grid. This report prices that rail, the legal-and-tariff path a developer needs to wheel power, in each market, then asks the harder question: what actually stands between a developer and a financed project.

Executive summary

- What a developer should take from this: In the five markets that can be fully costed, wheeled power already beats the grid by 20 to 60 percent. But a wide saving is not the same as a financed deal. For developers looking to build where the rail is finished and the money question is already settled: South Africa scales and Namibia for a single deal. Everywhere else, the cheap power helps but is not enough on its own, until a guarantee or a published charge closes the gap.

- The regulator's charge fixes the margin: The saving runs from 20.6 percent below the grid in Zambia to 60.5 percent in South Africa, and because the network fee drives that spread, a developer’s return is set by the charge a market chooses, not by the cost of its solar.

- The tariff rarely stops the deal: In five of the eleven markets, currency and sovereign risk are the binding constraints that only a development-bank guarantee clears; in four, the market is only partially open; in South Africa, it is a congested grid; in Namibia, it is only the sponsor and the buyer's credit.

- The map is moving: Within a year, Egypt generated roughly 400 megawatts of approved projects, South Africa's wholesale market will open in the third quarter of 2026, and the first wheeled deal will close, behind a development-bank guarantee, which would each move a market from waiting to working.

Ten markets allow wheeling; only six publish a usable price

Ten of the eleven markets here let a private generator sell across the grid to an industrial buyer, through laws as varied as South Africa's Electricity Regulation Amendment Act of 2024, Zambia's Open Access Regulations of 2024, Nigeria's Electricity Act of 2023, and Morocco's Law 13-09. Only Botswana, where the national utility is still the sole buyer and unbundling began only in July 2025, has no legal pathway at all.

Every market here is scored against four stages of readiness: a law that permits wheeling, a published charge a developer can quote, power actually flowing, and that flow at scale. Only one market clears all four:

Market | Status | Delivered $/kWh | Saving vs grid | What blocks a financed deal | Capital that unlocks it |

South Africa | Build today, at scale | 0.045 | 60.5% | Congested grid | Commercial |

Namibia | Build today | 0.078 | 38.8% | Sponsor and buyer credit | Commercial |

Zambia | Build today | 0.074 (lower bound) | 20.6% | Currency | Development bank |

Egypt | Rail-ready | 0.033 | 28.5% | Currency | Development bank |

Morocco | Rail-ready | 0.063 | 45.3% | No trading licence | Commercial, once licensed |

Nigeria | Rail-ready | not priced | — | Currency | Development bank |

Kenya | Half-built | not priced | — | No published charge | Awaiting a charge |

Ghana | Half-built | not priced | — | Currency | Development bank |

Zimbabwe | Half-built | not priced | — | Sovereign and currency | Development bank |

Tanzania | Half-built | not priced | — | No published charge | Awaiting a charge |

Botswana | Blocked | not priced | — | Monopoly utility | Awaiting unbundling |

Table 1. The eleven markets at a glance. Source: Electron Intelligence. Proxy or lower-bound inputs flagged; see Notes.

Enabling regulation is only the first requirement, and most of these markets clear it. What a developer needs before financing is a published network charge, because the network fee is the highest single cost in a wheeling deal, and without a regulated rate, it cannot be quoted or underwritten. That requirement removes four markets at once.

Kenya passed its open-access rules on 8 May 2026, but has not yet set a wheeling charge. Ghana publishes a transmission charge, but it applies to bulk utility customers, not to independent third-party supply. Zimbabwe quotes charges that have never been formally gazetted. Tanzania negotiates each charge on a case-by-case basis and keeps its transmission grid in state hands, closed to private third parties. In all four, wheeling is legal, but no usable transmission charge has been published, so a developer cannot price the highest cost in the deal.

Only three markets actually carry power

Legal (law permits) |

| ||

|

| ||

Published charge |

| ||

|

| ||

Carrying power |

| ||

|

| ||

At scale (one market) |

|

Source: Electron Intelligence

Figure 1. The path narrows at every stage: a law in ten markets, a published charge in six, real third-party flow in three, scale in one. Of the three, only South Africa and Namibia wheel home-grown generation; Zambia's flow is imported.

Passing a wheeling law is the start of the process, not proof that it works. The three markets that actually move power are South Africa, Zambia, and Namibia, and they show how different "operational" can be. South Africa has about six wheeling deals signed. The earliest are already switched on and delivering power, including Vodacom through SOLA Group and five Discovery Green contracts, such as Implats, with the rest coming online through 2026.

Zambia moves roughly 250 megawatts to its copper mines, but most of that power is imported to First Quantum across a drought-strained grid rather than generated at home and wheeled to a local buyer. Namibia is the cleanest small example, a single 10-megawatt contract from Maxwell to B2Gold's Otjikoto mine. All three are proven, though only South Africa operates at a real scale.

The network fee, not generation, sets the delivered price

In five markets, we can source all three inputs: the cost of generation, the network fee, and the grid tariff. For those, we calculate the delivered cost of wheeled power the same way we do in South Africa, and then compare it to the local grid tariff. Nigeria is the sixth market with a published charge, but its fees are hidden inside license orders, making it difficult to calculate the cost.

To compare the wheeling price and the utility tariff, we measure cost savings in local currency to remove the foreign-exchange impact.

Two caveats. First, we benchmark against the utility tariff, but in gas-rich markets like Nigeria and Egypt, a buyer's real alternative is often self-generation from diesel or gas, not the utility. Second, solar is intermittent, and making it reliable enough to depend on adds cost, so the real gap is narrower than the headline figure suggests.

What wheeled power costs, set against the grid

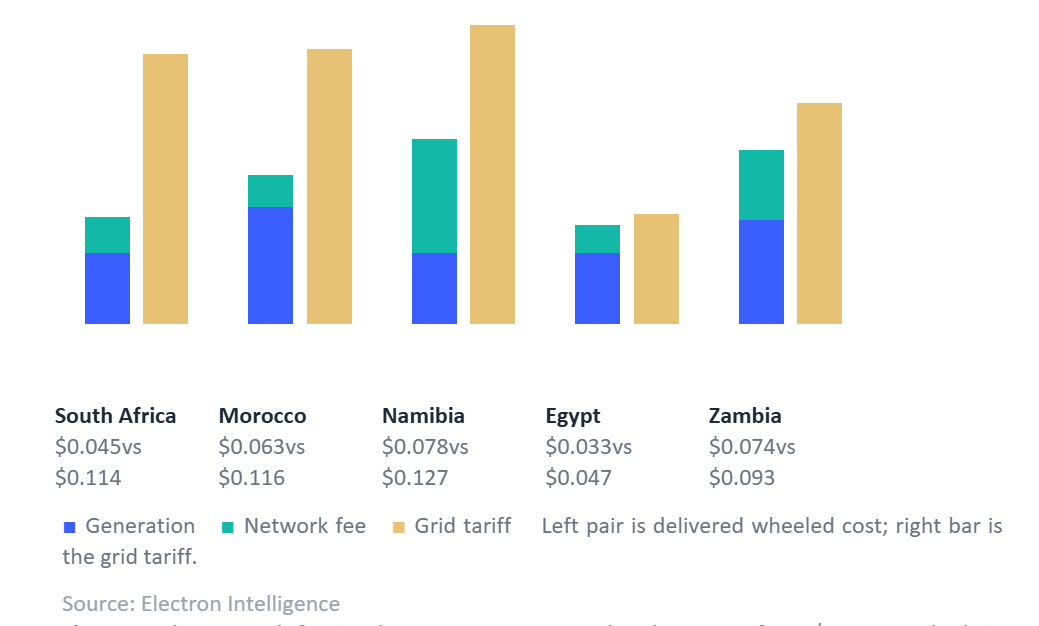

Figure 2. The network fee is what varies; generation barely moves, from $0.003 per kWh in Egypt to $0.048 in Namibia.

Generation costs are steady across the markets we can price, between about $0.030 and $0.050 per kilowatt-hour. The network fee varies and determines how each market compares with its utility tariff rate. Egypt charges almost nothing to move power, around $0.003, so even against its low grid tariff, wheeling still saves 28.5 percent. Namibia's small grid charges far more, about $0.048, which pulls an otherwise strong saving down to 38.8 percent. A regulator can change the network fee. It cannot change the cost of solar generation.

Where it can be priced, wheeling runs 20 to 60 percent below the grid

Every one of these savings would clear a lender’s hurdle on price alone, and the economics are not peculiar to South Africa.

How far wheeled power sits below the grid, by market

Saving on delivered wheeled cost against the grid industrial tariff, local-currency basis

South Africa |

|

| ||

|

|

| ||

Morocco |

|

| ||

|

|

| ||

Namibia |

|

| ||

|

|

| ||

Egypt |

|

| ||

|

|

| ||

Zambia |

|

|

Source: Electron Intelligence

Figure 3. Wherever the cost can be built up, wheeled power beats the grid by 20 to 60 percent. The savings travel across the continent; the working route does not, yet.

The savings show whether wheeling is economical, not where to build. The table answers that second question, because building depends on two conditions being in place: a working regulatory route and resolved financing. Developers should build now in the markets where both are settled and prepare in those where they are not. This measures each market's regulatory readiness, a separate question from whether a specific deal can be financed.

Morocco ranks second only to South Africa in price and needs only a trading license to reach a financeable deal. Egypt's savings are genuine but small: it charges almost nothing to move power, but its grid tariff is already held low by subsidy, which leaves little room to undercut.

The network fee determines the size of the savings, so the markets that are still setting their charges, Kenya and Tanzania, will fall somewhere between Egypt's small savings and South Africa's large ones. The level at which the regulator sets that charge will decide each market's competitiveness far more than the quality of its solar resource.

What stops a financed deal is usually the currency, not the tariff

Pricing the wheeling route indicates whether power can be moved and at what cost. It does not tell a lender whether the project will be funded. Across most of these markets, that depends on factors the wheeling charge has no bearing on. When the eleven markets are ranked by what stops a deal from being financed, rather than by the size of the saving, the order changes.

For nearly half the markets, the obstacle is the currency and counterparty payment risk, not the wheeling rail.

Currency and sovereign |

| ||

|

| ||

The rail itself |

| ||

|

| ||

A congested grid |

| ||

|

| ||

The deal itself |

|

Source: Electron Intelligence

Figure 4. Sorted by what actually blocks a financed project, the obstacle moves off the rail: the currency for five markets, the unfinished rail for four, the grid for South Africa, the deal for Namibia.

For five markets, the wall is the currency and the sovereign. Nigeria, Zambia, Egypt, Ghana, and Zimbabwe each carry a money problem larger than anything on the rail; so a wheeling charge and a wide saving are necessary and nowhere near enough. Zambia makes the point: it can build today, with power already reaching its mines, yet that power is imported and drought-exposed, and the kwacha is under strain, so a project there needs a political-risk guarantee and a dollar-linked contract, the work of a development bank rather than a developer. Zimbabwe is the same problem at its sharpest, where the sovereign itself is the question.

For four markets, the wall is the rail, still unfinished. Morocco, Kenya, Tanzania, and Botswana clear the money question but stop where the market is only partly opened, so the fix is a trading license, a published charge, or breaking up a monopoly, not a financing structure.

South Africa is an outlier. It is the one market where the wheeling framework is complete, so the binding obstacle is no longer regulation but the grid itself. The real cost there is curtailment: the network cannot carry all the generation connected to it. The fix is more transmission, more storage, and projects designed around congestion, not another round of legal reform.

Even calling the framework complete overstates it. Wheeling works smoothly on Eskom's national transmission network, but a deal that has to cross a municipal distribution grid still runs into trouble: municipal billing systems cannot account for wheeled power, and municipalities lose resale revenue when a customer wheels instead of buying from them. So the framework is more complete at the transmission level than at the municipal one.

Namibia is the one market where every major barrier has already been resolved, leaving only the ordinary commercial questions. Its dollar is pegged one-to-one to the South African rand, which minimizes the currency risk. What remains is the strength of the project's sponsor and the creditworthiness of its buyer, making Namibia the most bankable market of the eleven.

Each market sorts to the capital that can unlock it

For a developer, each market also fixes who you must bring to the table. In the five currency-bound markets, that partner is a development bank. The political-risk cover and hard-currency guarantee these deals need are things commercial capital cannot supply on its own: they do not lower the tariff; they absorb the sovereign and currency risk so that commercial debt can sit behind them. Without that cover, the savings are nothing. And that backstop can no longer be assumed.

Commercial infrastructure capital and private credit work best where the obstacles are smallest: Namibia, where only ordinary deal-level questions remain, and South Africa, where success depends on underwriting skill rather than country risk. In markets that are only partially open, there is nothing to invest in yet, and Morocco is the closest to changing that.

Where development-bank capital is what makes a deal possible, it increasingly comes with just-transition conditions, requirements to protect workers and coal-dependent communities, that a corporate wheeling deal does not meet on its own.

For the developer

For a developer, the work comes down to two tasks: choosing which market to enter, which the table answers, and structuring the individual deal, which it does not.

In markets where currency risk is the main obstacle, the developer should secure a buyer that is creditworthy and earns hard currency, denominate the power-purchase agreement in that hard currency, and bring in a political-risk guarantor while the deal is being structured rather than afterward.

The cost-saving needs protecting, too. That means fixing the wheeling and standby charges for the full term of the contract, favoring buyers connected directly to Eskom's transmission network over those behind a municipal distribution grid, and sizing the deal against the firm delivered cost of power, which includes the cost of making intermittent solar reliable, rather than against the headline saving.

What we are watching

Egypt is the closest to activating. About 400 megawatts of approved projects will come online the day the first plant switches on, though currency remains the obstacle there.

Kenya's regulator has yet to set its wheeling charge, and that single decision is what would make the market priceable.

In the currency-bound markets, the clearest signal will be the first wheeled deal closed behind a political-risk guarantee, which would prove the financing route the other five markets are waiting on.

South Africa has become the first market to move from a wheeling problem to a grid problem, and rising curtailment is where that shows. Its response is institutional: the wholesale electricity market, now delayed from April to the third quarter of 2026, together with the grid-capacity-allocation rules the regulator approved in November 2025.

The wheeling charge itself is the final variable to consider, because it determines the size of the savings. As Eskom and the municipalities lose sales volume to private power, the pressure to raise network and standby charges to protect their revenue will grow. Cost-reflective tariff reform could therefore narrow the savings from the other side, even in markets where wheeling already works.

Bottom line

Wheeling is a reality in South Africa and, almost everywhere else, still only a possibility. The savings hold in every market that can be costed, so the economics are not the obstacle. Three markets carry power today, but only two, South Africa and Namibia, can finance a deal without outside help; every other market is waiting on a first deal or a guarantee. What ultimately determines whether a deal gets financed is the country, not the tariff: its currency, its solvency, its grid. The savings tell a developer that wheeling is worth doing, while the obstacle tells the financier what it will take, and those two answers are rarely the same.