Wholesale to Retail: South Africa's Energy Capital After JETP

How the collapse of South Africa's energy transition financing shifted bankability from a programme-level guarantee to a deal-by-deal problem

In 2021, the G7 and the European Union pledged $13.8 billion to South Africa's Just Energy Transition Partnership (JETP). The capital mattered, but the larger purpose was to solve bankability at scale. One framework carried multilateral political capital, de-risked the sector for private finance, and placed Eskom, the state utility, at the centre as the single creditworthy counterparty for the whole financing chain.

That framework broke in two stages. In 2023 the National Treasury imposed a borrowing moratorium on Eskom as the price of $14 billion (R254 billion) in debt relief. In February 2025, the United States withdrew $1.056 billion and removed the political structure holding the partnership together. What followed was not a slower transition but a different one: bilateral, uncoordinated, and more expensive at every step, with three vehicles now racing to solve in retail what the JETP was solving wholesale.

Executive Summary

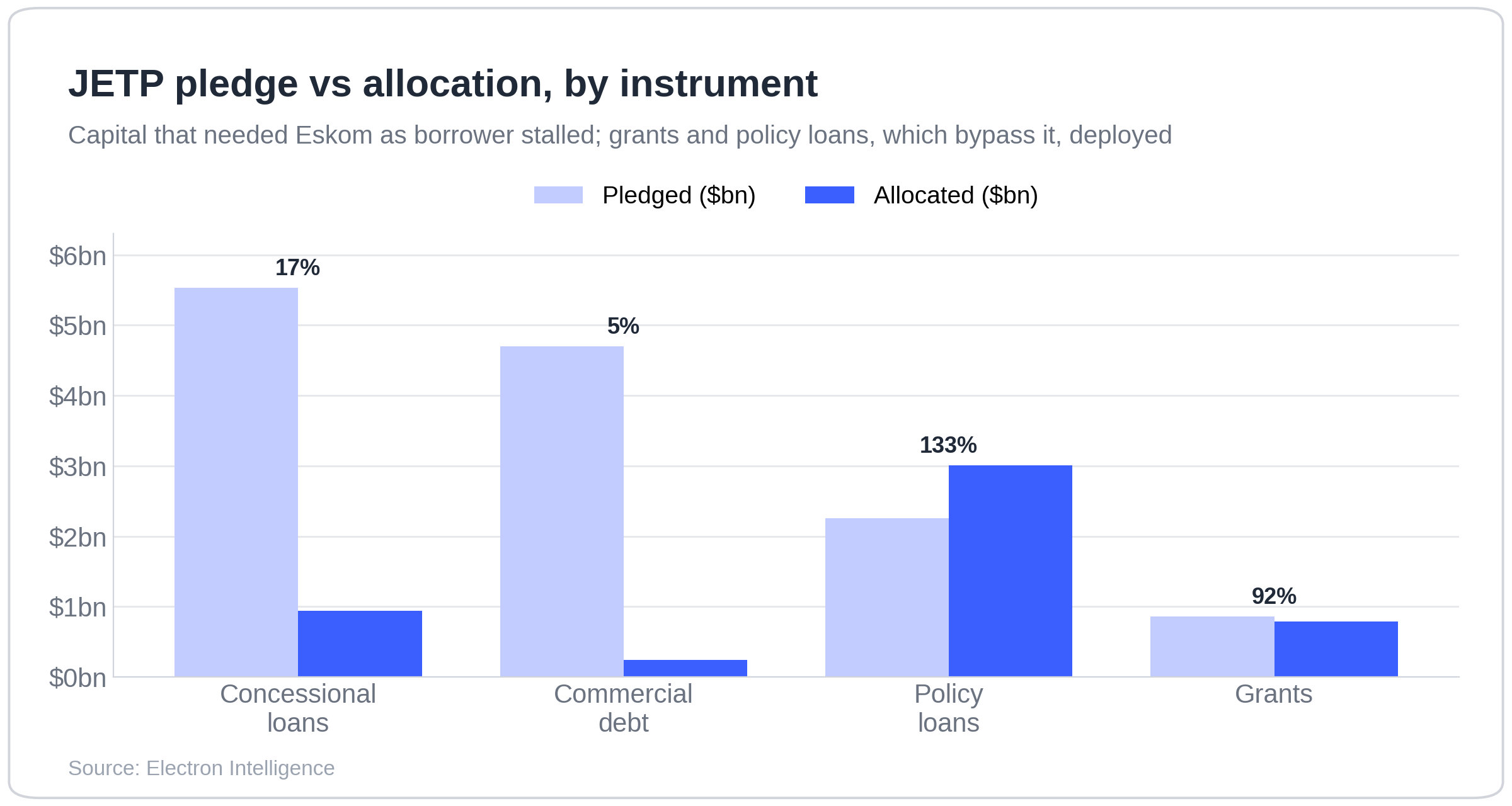

The JETP's value was coordination, not just capital. It made the transition readable to private markets, held the government aligned across ministries, and named Eskom as the counterparty that would absorb the financing. The 39% allocation rate on the post-exit pledge base is the lost coordination shown in the data.

Bankability has inverted. Eskom was built to be the creditworthy anchor of the transition. It is now the risk new vehicles are designed to avoid: direct municipal lending, the Credit Guarantee Vehicle (CGV) for transmission, and Eskom Green, a ring-fenced subsidiary for new renewables. Each covers only one part.

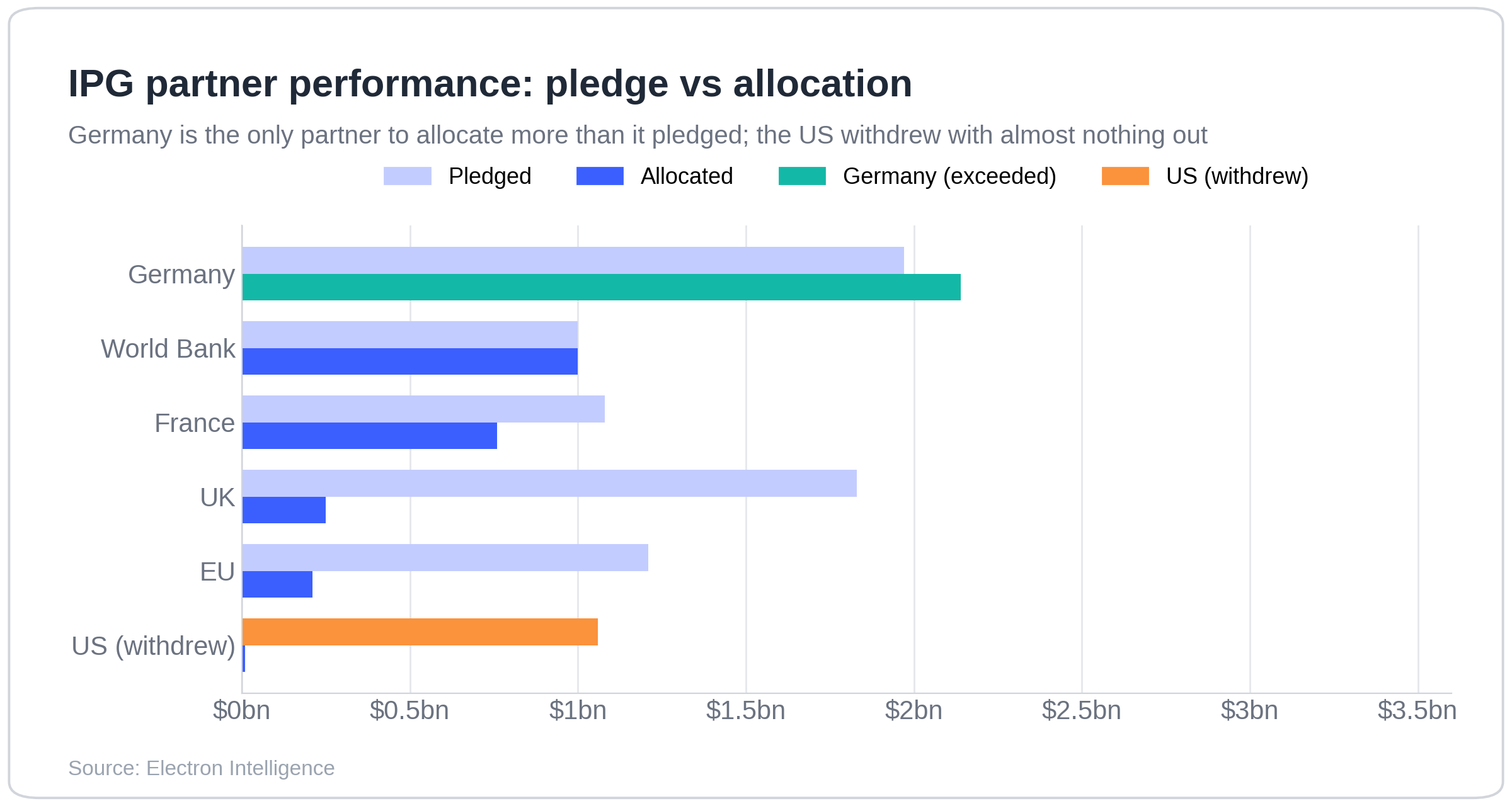

The retail model works only where municipal credit is strong, and that pool is thin. KfW, the German state development bank, lent $160 million (R2.9 billion) to Cape Town in February 2025 and $210 million (R3.8 billion) to Johannesburg in May 2026, both on the cities' own credit with no Eskom counterparty. Germany is the only member of the International Partners Group (IPG) to exceed its original pledge.

Eskom Green is the most consequential vehicle and the least settled. Separated from Eskom's balance sheet, it offers KfW and the European Investment Bank (EIB) clean exposure to new assets. But in October 2025 private producers asked the Competition Commission whether it can jump the grid-connection queue ahead of them.

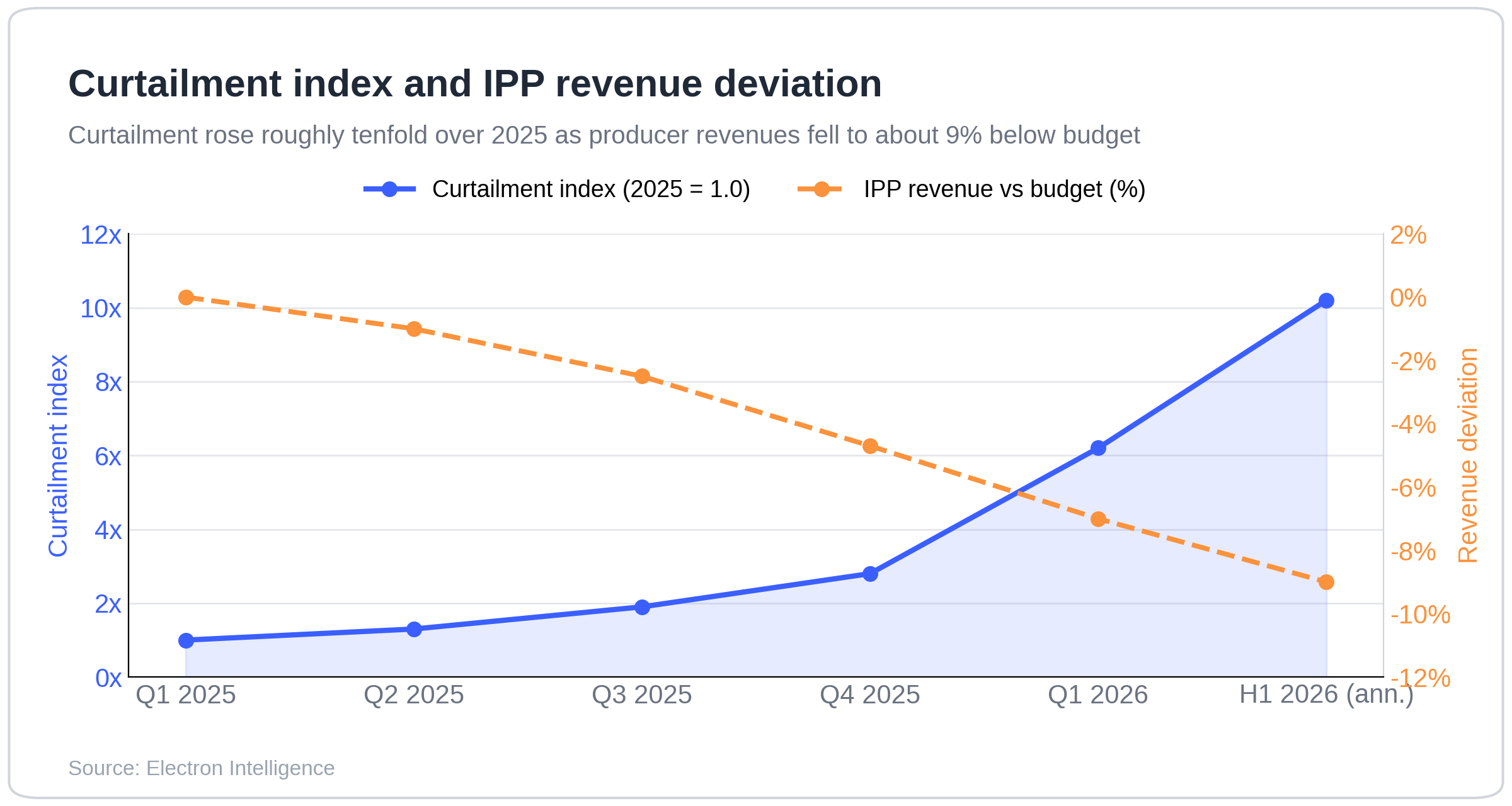

Curtailment is the first live cost. In the first half of 2026 Eskom curtailed independent power producers at roughly ten times the full-year 2025 volume, and sector revenues ran 9% below budget. The market has not fully priced it.

What the JETP Did, and How It Broke

The JETP was a coordination mechanism with capital attached. It signalled that the transition was real, backed at the highest level, and run through a defined framework with named counterparties, which made private capital willing to follow. The design rested on Eskom. As national utility, grid operator, and the buyer under every power purchase agreement (PPA) in the Renewable Energy Independent Power Producer Procurement Programme (REIPPPP), Eskom had to stay creditworthy and able to borrow. Both conditions were already under strain before the moratorium formalised the problem.

Bankability for generation did not begin with the JETP. The REIPPPP established it in 2011 through three contracts: a standardised twenty-year PPA, an Implementation Agreement under which the Treasury stood behind Eskom's payments, and a Direct Agreement giving lenders step-in rights on default. That structure carried the first four bid windows to financial close years before the JETP existed. Nor was the partnership the bulk of the money. Its IPG pledge equalled 8.6% of the $98.7 billion (R1.48 trillion) the transition needs, at the original $8.5 billion level, and only about 4% of that came as grants. What it promised to add was coordination over a working backbone, not the backbone itself.

The breaks formalised an underperformance that was already there. In 2023 the Treasury moved $14 billion (R254 billion, later trimmed to R230 billion) of Eskom debt onto its own balance sheet, and the price was a moratorium barring new Eskom borrowing until the end of the 2025/26 financial year, on 31 March 2026. The concessional project loans channelled through the Just Energy Transition Project Management Unit (JET PMU) had no eligible borrower, because Eskom was the intended one. The US exit in February 2025 then forfeited $56 million in grants and $1 billion in finance from the US International Development Finance Corporation, and cost the partnership its leverage in Pretoria. Disbursement had lagged from the start in any case, held back by a shortage of investable projects and a domestic fight over pace. Only one coal station has closed, and Camden, Grootvlei, and Hendrina have slipped to 2030 and beyond. Indonesia and Vietnam show the same pattern.

The 39% allocation rate at mid-2025 maps the damage. Grants and policy loans, which reach the Treasury without an Eskom counterparty, were deployed well above average. Concessional project loans, which needed Eskom as the borrower, deployed near zero. By the end of 2025, 248 projects had nudged the rate to 43%, with more grants moving rather than any fix. The present risk follows directly. The Treasury-backed PPA still covers an Eskom default, but it does not cover curtailment or Eskom competing for the same grid, and that is where revenue now leaks.

Three Vehicles, One Missing Counterparty

Three vehicles now compete to supply what Eskom once supplied. Direct municipal lending is the only one with a completed deal record. Johannesburg and Cape Town qualified on their own balance sheets and took KfW facilities without routing through the JET PMU: $210 million (R3.8 billion) for Johannesburg in May 2026 and $160 million (R2.9 billion) for Cape Town in February 2025, neither secured on city assets. Germany's total commitment has reached $2.95 billion (EUR 2.68 billion) against a $1.1 billion (EUR 986 million) original pledge, with a further $550 million (EUR 500 million) policy loan to the Treasury in July 2025. The limit is the size of the pool. Buffalo City, Mangaung and Nelson Mandela Bay do not qualify unenhanced, and whether the EIB, France's AFD and UK Export Finance extend the model is the open question.

Transmission is the largest single gap, at least $18 billion (R321 billion, more on some estimates) by 2032, and generation that cannot reach the grid earns nothing. The CGV is the instrument aimed at it. The World Bank backed it on 5 March 2026, a partial guarantee capitalised with $350 million from the Bank's lending arm plus an initial Treasury contribution. But a guarantee is not a fund. Its roughly $10 billion ten-year mobilisation target spans infrastructure broadly, and its first transmission tranche covers seven corridors worth about $1 billion, an order of magnitude short of the gap. It becomes operational only in the second half of 2026, and nothing has yet been drawn.

Eskom Green launched on 9 June 2026, ring-fencing new generation from Eskom Holdings' balance sheet so co-investors get clean exposure rather than the parent's legacy debt. It targets 32 GW by 2040, with 6 GW by 2030 and 2 GW under way. The structure is sound. The open question is whether it behaves as a genuine new entrant or uses Eskom's position as grid operator to take advantages private producers cannot, which is what the grid-allocation process must resolve.

Fragmentation Priced in Real Time

All three vehicles run on a strained grid. In the first half of 2026 Eskom curtailed independent producers at roughly ten times what it curtailed in all of 2025, and revenues tracked 9% below budget. Congestion, delayed transmission and Eskom's control over dispatch all contributed, but the deeper problem is structural: Eskom decides who generates and when, and through Eskom Green it is now a competitor.

For existing REIPPPP projects across Bid Windows 4 to 6, this cuts revenue directly. The PPAs pay for each megawatt-hour delivered, not for what a plant could have produced, and curtailment losses fall outside the contract's cost-adjustment mechanisms and outside the Treasury guarantee, which covers default, not dispatch. The reimbursement backlog is approaching $56 million (R1 billion), with delays of up to a year. For developers underwriting Bid Window 7, commercial-and-industrial or merchant projects, grid node and queue position have become front-line inputs, and curtailment is repricing deals now, well ahead of the 2031 target for competitive dispatch. In October 2025 the producers' association asked the Competition Commission whether Eskom Green's pipeline, clustered near retiring coal stations, lets it jump that queue. The ruling is pending.

Part of this fragmentation is reform working as intended. The Electricity Regulation Amendment Act took effect on 1 January 2026, the transmission business is now a separate company, the National Transmission Company, and the single-buyer model is giving way to a competitive market, with the Wholesale Market Code phasing in through 2026. The end of Eskom as the one counterparty is not only an accident of the moratorium and the US exit. It is national policy. The question for investors is whether the reform arrives before the counterparty vacuum is priced into too many curtailed or stranded assets.

Where the Cost Lands

The capital has not left; the coordination has, and the cost now surfaces at a different point for each kind of lender. For development finance institutions, it appears as a replication problem, since the municipal template that works for Cape Town and Johannesburg does not reach the secondary cities. For commercial banks, it is a pricing question, with those same facilities offering a senior-debt structure that carries no Eskom counterparty. For investors holding Bid Window 4 to 6 assets it lands in the revenue line, where curtailment sits outside both the contract's adjustment mechanisms and the Treasury guarantee. For developers, it lands in underwriting, as grid node and queue position displace the offtake counterparty as the variable that decides a project. The single point of risk that Eskom once absorbed is now spread across all four.

What We're Watching

Moratorium expiry and the first Eskom Green co-investments

The moratorium lapsed in March 2026, and Eskom can borrow again, though from a weak credit position. If UKEF, AFD and the EU facility managers co-invest in Eskom Green in the first half of 2027, the ring-fenced model becomes the post-moratorium channel. If they hold back, municipal lending consolidates as the default.

The CGV's first draw

A draw for a secondary municipality would extend direct lending beyond Johannesburg and Cape Town. A draw at the transmission level would move the programme from design into deployment. No draw by mid-2027 means the gap widens faster than the instrument built to close it.

The grid-access ruling

The Competition Commission's response decides whether Eskom Green queues on the same rules as private producers. A ruling in their favour lets Bid Window 7 developers model grid access on equal terms. The grid positions are being set now.

Bottom Line

The municipal model works but reaches only two cities. The CGV has not drawn against a transmission gap of at least $18 billion (R321 billion). Eskom Green offers clean exposure but carries an unresolved competitive structure. None of the three coordinates with the others, and none reaches the full pool the JETP was built to serve. Curtailment at ten times last year is the transition pricing its own fragmentation in real time, and revenue models written before the moratorium, the US exit, and Eskom Green are working from a single-counterparty structure that policy is dismantling and the market has already left behind.